Why You Should Not Loose Time in 🐢Europe as a Startup

Roll-Right-In Podcast - Key Insights From the StudioAlpha Accelerator

Go where the money is 💰: Headquartered in Zurich and partnering with Atlassian in San Francisco, we were in both worlds at home. Over the years, based on revenues of our apps, we realized that Jira adoption in the USA was rapid, pragmatic and widespread vs. Europe lacked about 10 years behind. European engineering teams having a hard time to convince their supervisors, who in turn, had to struggle with lengthy internal authorization processes, still often ruled by non-tech people.

Aiming for USA, the biggest market in the world, was a game-changer for us. Here are compelling reasons why European founders should think about flipping their startups to the US.

A brief overview that takes 5 minutes to read.

Productivity in Europe has weakened 🐨: In the fourth quarter, eurozone productivity fell by 1.2% from the previous year, contrasting with a 2.6% rise in US productivity over the same period. This trend reflects a longer-term pattern where US labor productivity growth has more than doubled that of the eurozone and the UK over the past two decades.

How come? Several factors contribute to this divergence, including differences in demographics, with the US benefiting from a younger, faster-growing population that works longer hours. Additionally, the US's higher output per hour worked points to more effective production processes. European's inability to match the US in private and public sector investments, particularly in the wake of challenges like increased energy prices due to geopolitical tensions and the fragmented nature of its financial and regulatory environment makes things worse.

🤔 Things that make you go hmmmm? - Let’s delve a little deeper.

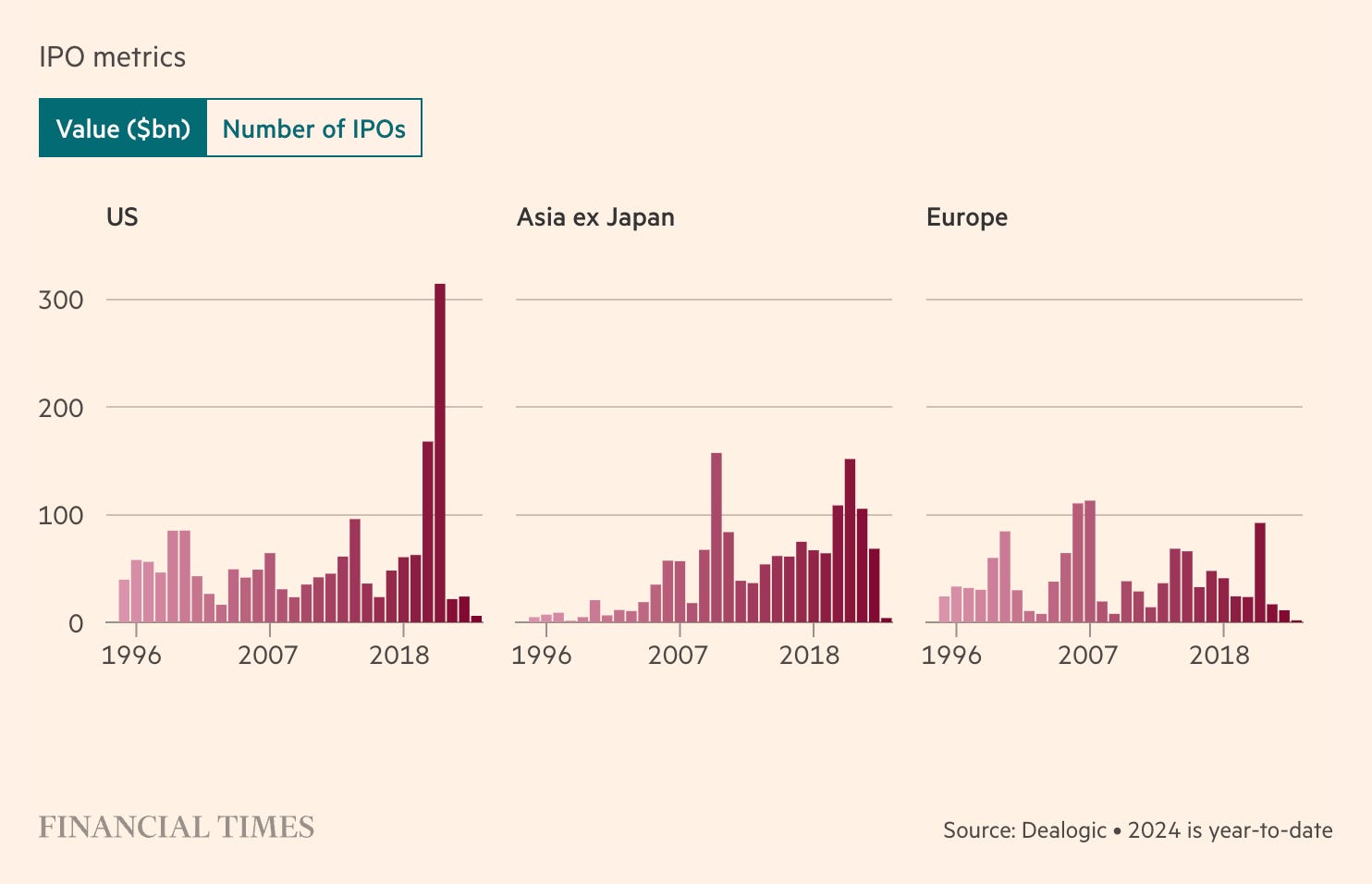

European financial markets have weakened, too 🐨🐨: Despite record highs in market indices, Europe’s equity markets face a hidden turmoil. Trading volumes are dwindling, IPOs are few and far between, and the continent's corporate giants often look westward to the US markets.

Historically, the performance of European and US stock markets mirrored each other closely, with Europe's pace slightly trailing behind that of Wall Street. However, post-2008, a stark divergence emerged. While the US market soared, propelled by the technological juggernauts of Silicon Valley, Europe's markets languished, failing to capture the same level of investment enthusiasm. The American tech sector's explosive growth not only reshaped its own market but also recalibrated global financial flows, solidifying a virtuous cycle of wealth and innovation concentration.

The urgency of this situation has sparked a call to action among European policymakers. The goal? To rejuvenate local markets, bolster investment in homegrown companies, and galvanize businesses to pursue local listings. Yet, this ambition grapples with entrenched political, financial, and cultural challenges that have long hindered progress. Meanwhile, the US market's allure only grows stronger. We don’t expect a change any time soon.

Europe's Tech Deficit 👨🏼🌾: Europe’s markets lack the 'Silicon Valley rocket fuel'—the dearth of rapidly scaling tech firms compared to the US has left its indices less dynamic. Economic growth has been tepid, and the appetite for risk among European investors is noticeably lower. Without the zeal to back startups that are still maturing into profitability, Europe’s market vitality has suffered. Meanwhile, new financial powerhouses like China and India are fostering vibrant capital markets of their own, underscoring the competitive global landscape. Europe has also fallen behind Asia.

Too, Europe’s corporates fall behind 🐢: The FTSE 100 is an index consisting of the shares of the 100 biggest companies by market capitalization on the London Stock Exchange. Meanwhile, it is smaller than Microsoft. The DAX, a stock index that represents 40 of the largest and most liquid German companies has briefly been overtaken by Nvidia on the right.

Pic: FT

Why make it simple when it can be complicated 😵💫: This saying hits the nail on the head. While the US enjoys a relatively streamlined market architecture, Europe's financial landscape is a mosaic of complexity. Almost every European nation prides itself on having its own stock exchange, fragmenting liquidity and complicating post-trade activities.

Tab: Data FT

Cultural Contrasts in Investment 🎰: The investment ethos in Europe starkly contrasts with that of the US. Where American retail investment culture has burgeoned, particularly with the rise of meme stocks during the pandemic, Europe remains cautious. European households lean towards cash savings over equity investment, further indicating a divergence in retail investment culture.

Many European pension funds, including those in Switzerland, have yet to significantly engage in startup investments and are not expected to do so anytime soon.

Why Silicon Valley Matters: Our narrative, reflected in the current StudioAlpha batch, underscores a critical truth: comprehending the dynamics of Silicon Valley is essential for global tech entrepreneurship. The US, particularly Silicon Valley, continues to be the fulcrum of tech innovation and investment. Understanding this ecosystem is crucial for entrepreneurs aiming to align with the expectations of global tech investors.

How many languages are you speaking? OR ‘Why make it simple when it can be complicated’ part 2 😵💫😵💫: Most statistics compare the USA with ‘Europe’, which is misleading. Europe comprises 47 countries, each with its own jurisdiction (i.e. 47 different tax laws) and encompasses 150-200 languages and even more diverse cultures. Additionally, increasing segregating energies make it extremely challenging for startups to expand within the European market.

Will the future be better for Europe 🥳? - Hmmmm …, good question. European politicians once optimistic about leading the IoT (Internet of Things) after conceding the Internet's first half to the US. But that never really happened and this is the reason why US companies dominate meanwhile 86% of the software market worldwide.

European countries are now facing the rapid shift in technological focus to AI, with San Francisco's Hayes Valley, or "Cerebral Valley," at the forefront of AI startup innovation … without talking about Nvidia & friends. This vibrant district has become a hub for AI talents living and working together in "hacker houses," fostering an intense culture of innovation. Despite these advancements, European press often highlights San Francisco's challenges, such as homelessness, overshadowing the city's tech achievements. However, SF is doing extremely well when it comes to the future of start-ups and innovation. It looks like SF will also emerge from the post-COVID era stronger than alternative hubs in the USA.

And finally this: It's clear that Europe has a history of focusing on regulation, which can be seen in its approach to digital markets and technologies. While the US is often credited with pioneering new technologies, Europe prides itself on setting regulatory standards that often shape global practices. However, this regulatory emphasis might contribute to the perception that Europe is lagging in fostering innovation and generating wealth compared to the US. The introduction of the EU AI Act is a recent example, highlighting Europe's preference for regulation over innovation. This act aims to address the ethical and safety concerns associated with AI but also raises questions about its impact on Europe's competitive edge in the rapidly evolving tech landscape.

Pic: “Shaping Europe’s Digital Future”: What is the personal contribution of these three individuals to the GDP?

Conclusion: The state of Europe's markets serves as a cautionary tale of fragmentation and conservatism in the face of global market dynamics. Instead of further EU regulatory fury the need for cohesive policy action is clear as the continent strives to catalyze its financial sectors and unlock the full potential of its markets. As European policymakers chart a course for revival, the journey ahead demands strategic alignment, cultural shifts, and a bold reimagining of the European investment paradigm. That will take at least 10 years to be corrected.

Well, that’s it for now. Thank you for reading and posting your questions and feedback!

Stay tuned for further insights and stories.

Best,

Fabian from Switzerland

LinkedIn | Insta | Twitter

🎙️ Path to Silicon Valley: What It Takes to Be Investor-Ready

Roll-Right-In Podcast with Daniel Parames, Partner Cooley Lawyers, San Francisco

Among others our lessons learned are the foundation of StudioAlpha's accelerator. Currently, we're in the middle of our 10-week sprint spring batch.

Embracing the Silicon Valley Mindset with Daniel Parames: This podcast episode featuring Daniel Parames unpacks what it means to be 'Silicon Valley-ready.' This conversation isn’t theoretical; it's a distilled essence of startup success narratives. For any tech entrepreneur aiming globally, grasping the Silicon Valley ecosystem's nuances is indispensable. Watch now:

Harness our journey—learn from our experiences and our missteps. Join StudioAlpha's accelerator program for not just investment but a real shot at Silicon Valley readiness. Our accelerator is a gateway to pitch directly to top investors in San Francisco 🌉. Watch our podcasts and get inspired.

Pic: StudioAlpha

Sources:

Financial Times, Europe faces ‘competitiveness crisis’ as US widens productivity gap, March 9, 2024

Financial Times, In charts: why European stock markets are in crisis, March 3, 2024

Peter Oppenheimer, Chief Global Equity Strategist, Goldman Sachs (CNBC, 10/1/2024)

The San Francisco Standard, What is ‘Cerebral Valley’? San Francisco’s nerdiest new neighborhood, January 13, 2023

Graphics: https://www.evolutionizer.com/blog/business-challenge-no1 ; adjustments by StudioAlpha

https://www.visualcapitalist.com/us-companies-global-markets/

https://digital-strategy.ec.europa.eu/en/news/eu-and-us-continue-strong-trade-and-technology-cooperation-time-global-challenges

StudioAlpha: Reflecting on our journey shared last year about our company beecom, our saga of evolution, failures, perseverance, innovation, and strategic transitions remains pivotal for emerging entrepreneur. Dive back into that narrative here.

The best is to invest in European talent that call Silicon Valley their home... That's what we are doing at www.diaspora.vc

Lies, damn lies, and comparing inflation statistics

UBS Weekly Blog by Paul Donovan

Financial markets seem to believe a story about divergent inflation risks between Europe and the United States. European inflation has slowed to 2.4%, while US consumer price inflation is 3.5%.

The reality is that while the Euro area had 2.4% y/y inflation in March, the US also had 2.4% y/y inflation in March—using the US harmonized inflation measure. US harmonized inflation adopts the same method as Europe to calculate inflation—it is a like-for-like comparison. The US harmonized measure does include some price discounts that the Europeans do not, but this is a minor difference. Using the respective harmonized core inflation measures, US inflation is notably lower than that of the Euro area.

Current differences between headline US and European inflation are thus more about calculation methods than inflation realities. Headline US inflation is dominated by the fantasy price of owners’ equivalent rent, and owners’ equivalent rent is not allowed anywhere near either European or US harmonized inflation data.

Identical US and European inflation on a like-for like basis does not prevent central bank policy divergence. The US Federal Reserve does not focus on the international harmonized inflation measure as a target. However, the similar real-world inflation experience does raise questions about the economic consequences of any policy divergence.