When Markets Rise While Wars Continue

Why AI, oil, trade and fear are pulling markets in different directions

Ukraine is unresolved. Iran is unresolved. Oil is volatile. Shipping routes remain exposed.

At the same time, markets have kept rising.

That looks wrong.

It may not be.

There is an old investor line about buying when cannons fire. The harder question is what markets are actually buying when the world looks less stable, not more.1

1) War is not one economic event

The word “war” covers too much.

A regional oil shock, a European land war, a naval blockade, a cyberattack, and a direct conflict between major powers are not the same economic event.

They may all create fear. But they do not hit the economy in the same way.

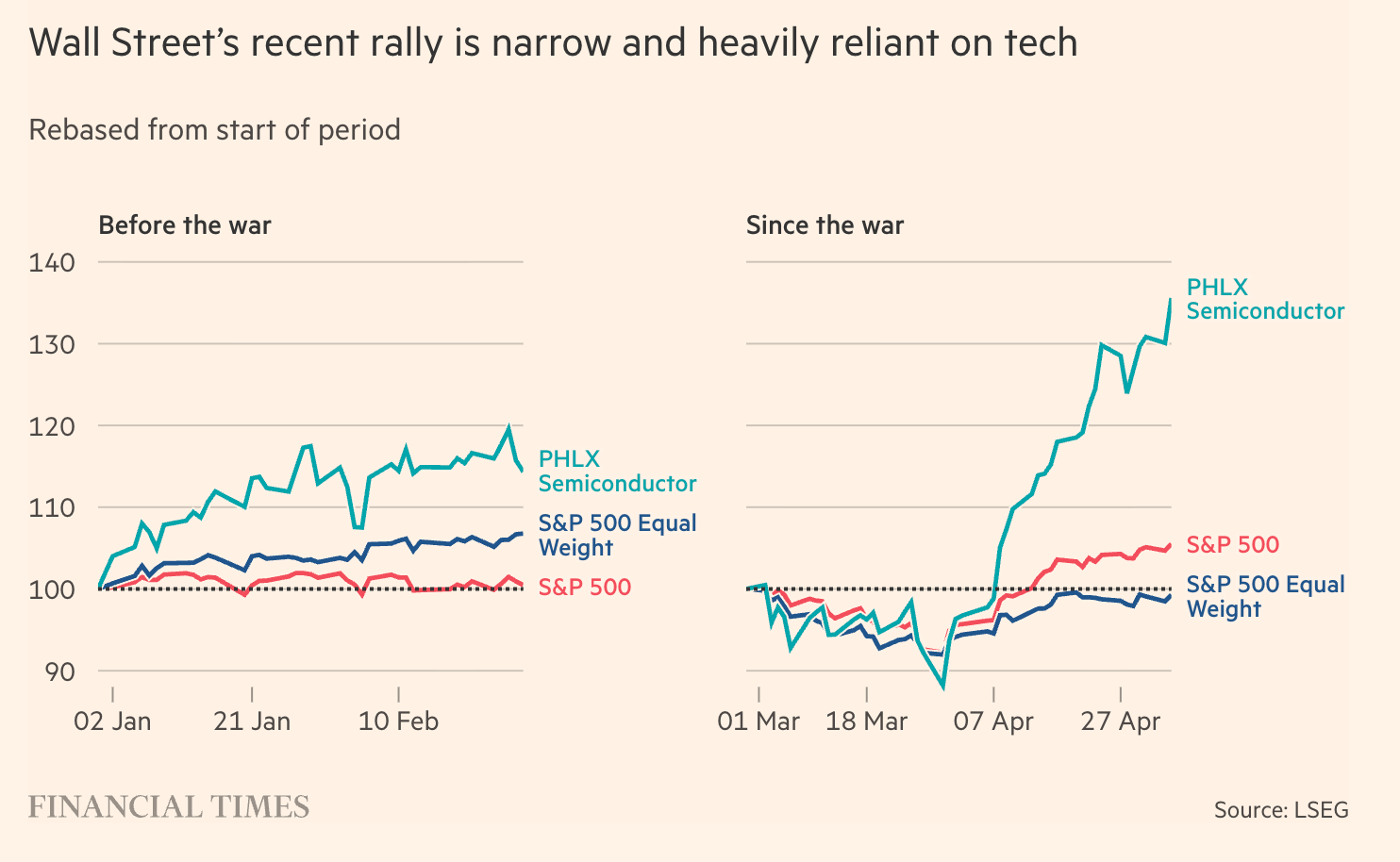

The FT’s latest chart analysis makes this visible. Since the Iran war began, the world’s biggest listed companies have added about $5.4 trillion in value. But this is not broad market calm. Semiconductor companies with market values above $10 billion gained $3.7 trillion, while airlines, consumer goods companies, carmakers, miners and several defence groups came under pressure.2

For markets, the relevant question is narrower:

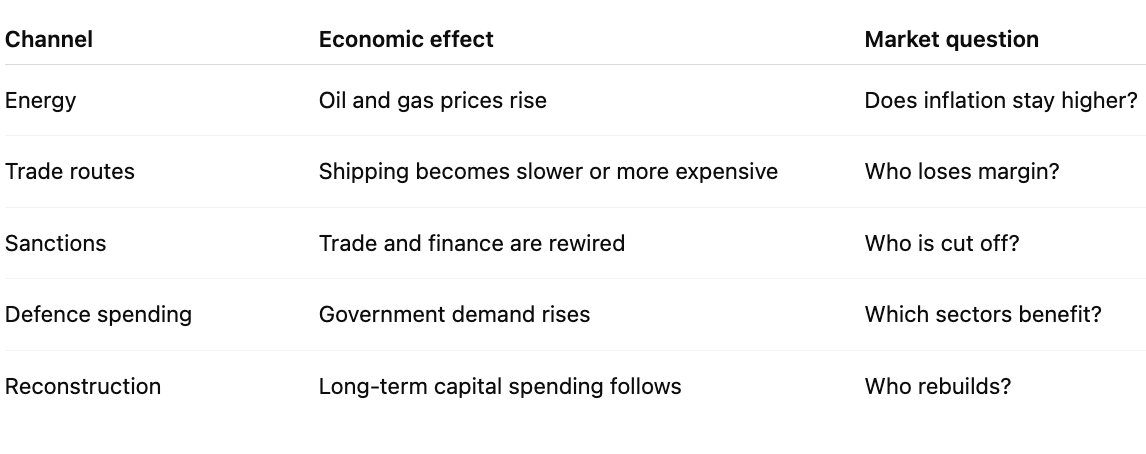

Which economic channel is being hit?

Ukraine and Iran sit in different parts of this table.

Ukraine has become an energy, fiscal, food, defence and reconstruction story.

Iran is more directly an oil, shipping, inflation and escalation story.

That difference matters.

This also explains why markets can look calm when the world is not calm.

Markets are not designed to measure suffering. They measure claims on future cash flows. A war can be a human disaster and still not immediately break the profit outlook for the largest listed companies.

At the moment, AI and chip stocks are the larger force at index level. That does not mean the war has no economic cost. It means the cost is showing up unevenly.

This is not broad calm. It is selective pricing.3

2) 🇺🇦 Ukraine: the long economic shadow

Ukraine shows how war becomes a balance sheet problem.

The first market shock in 2022 was only one phase. The longer economic effects came through energy prices, food prices, sanctions, fiscal support, migration, infrastructure damage, defence spending and reconstruction.

The World Bank’s latest assessment, prepared with the Ukrainian government, the European Commission and the United Nations, estimates Ukraine’s reconstruction and recovery needs at almost $588 billion over the next decade. That is nearly three times Ukraine’s estimated nominal GDP for 2025.4

The same assessment estimates direct damage at around $195 billion, with housing, transport and energy among the worst-hit sectors.5

That is the economic structure of a long war.

It is not only destroyed buildings. It is damaged power generation, broken logistics, weaker public finances, labour displacement, higher insurance costs, and years of capital allocation into repair rather than growth.

For Europe, Ukraine also exposed a dependency that had been underestimated for years: cheap imported energy.

Once that assumption broke, the shock moved from geopolitics into electricity prices, industrial margins, household budgets and central bank policy.

War becomes economically powerful when it touches an existing dependency.

3) 🇮🇷 Iran: the oil channel

Iran is different.

The market does not need to price a global war to worry about Iran. It only needs to price oil, shipping, inflation and escalation risk.

Reuters reported that oil prices rose as talks with Iran stalled, while U.S. equities still edged higher because AI and chip strength remained the dominant market force.6

The economic chain is direct:

Iran → oil → inflation → rates → valuations

Higher oil prices can squeeze consumers, airlines, logistics firms and energy-intensive industries. They can also support energy stocks. If oil keeps inflation higher, central banks have less room to cut rates. If rates stay higher, equity valuations become harder to defend.

This is why Iran can matter even for companies with no direct exposure to Iran.

The channel is macro, not local.

4) Trade may reduce war. Decoupling changes the calculation.

Soumaya Keynes’ recent Financial Times column is a useful entry point into the deeper question.

The column revisits Norman Angell, the British writer often mocked for supposedly arguing before the First World War that trade had made war impossible.

That version is too simple. Angell later won the Nobel Peace Prize in 1933. The irony is that he is remembered mostly for being “wrong” before World War I, although his real argument was not that war was impossible, but that modern war had become economically self-defeating.7

Angell’s actual argument was more careful. War was not impossible. War had become economically irrational. Trade had made conflict more expensive and conquest less useful.8

A new NBER working paper by Ling Feng, Qiuyue Huang, Zhiyuan Li and Christopher M. Meissner tests a related idea with modern data.

The paper studies global bilateral data from 1962 to 2014. To address the problem that peace itself may cause trade, the authors use changes in air transport technology as a way to isolate the effect of trade on conflict. Their result: increased trade significantly reduces both the probability and intensity of conflict between countries.9

The paper calls this the “peace dividend” of international trade.

The mechanism is straightforward. When two countries trade heavily, conflict becomes more expensive. Firms lose customers. Consumers lose supply. Governments lose tax revenue. Sanctions become more powerful.

That does not mean trade guarantees peace. It clearly does not.

It also does not mean every dependency is healthy. Some dependencies become strategic vulnerabilities.

But the argument creates a serious tension for today’s world.

Governments want more resilient supply chains. They want fewer critical dependencies on rivals. They want to reduce exposure to countries they no longer trust.

That is understandable.

But removing economic links can also reduce one layer of deterrence.

De-risking may make countries safer in one way and more exposed in another.

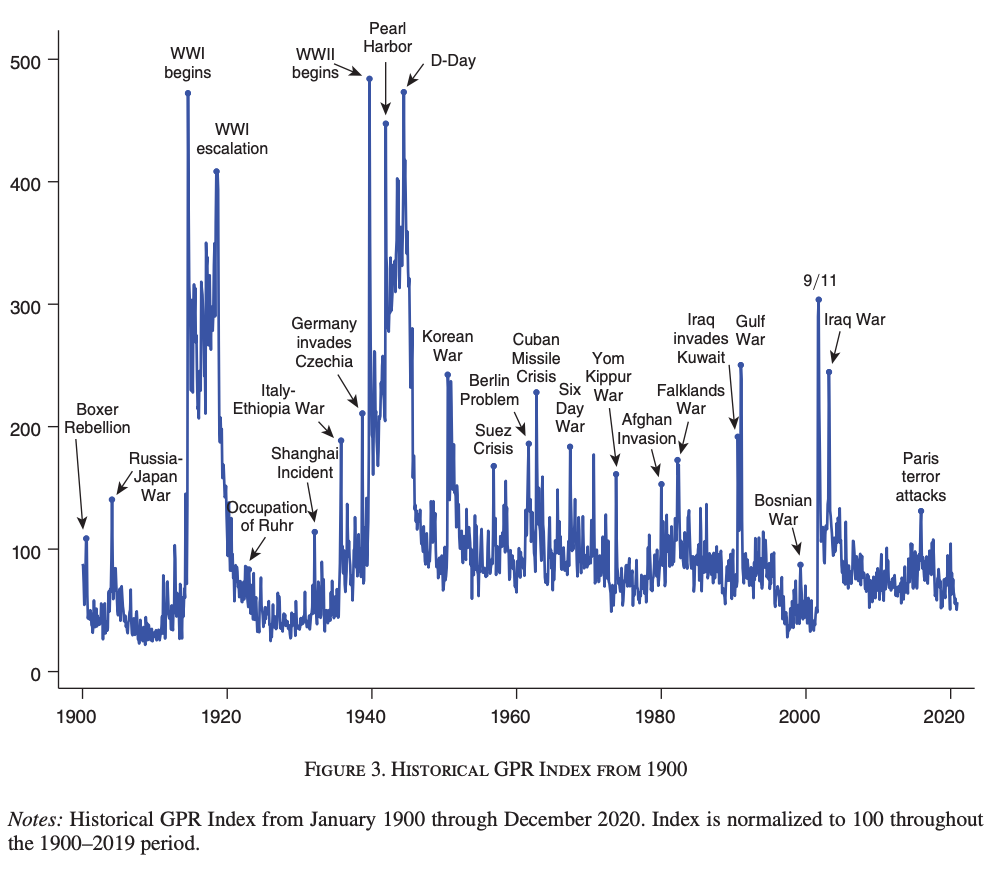

5) Geopolitical risk (GPR) still has a cost

The fact that markets can rise during conflict does not mean geopolitical risk is harmless.

Dario Caldara and Matteo Iacoviello’s Geopolitical Risk Index (GPR Index), published in the American Economic Review, measures adverse geopolitical events and related risks using news data. Their work finds that higher geopolitical risk foreshadows lower investment and employment and is associated with larger downside risks.10

This matters because geopolitical risk often works through hesitation.

Companies delay investment.

Boards postpone expansion.

Consumers become more cautious.

Investors demand higher returns.

Governments allocate more money to defence and less to other priorities.

The effect is not always immediate. It can accumulate.

This also explains why index levels can mislead.

The S&P 500 and Nasdaq can rise while parts of the real economy absorb new friction. A small number of large AI and chip companies can pull the index higher while airlines, industrial firms, retailers or European manufacturers face a more difficult cost environment.

The index is not the economy.

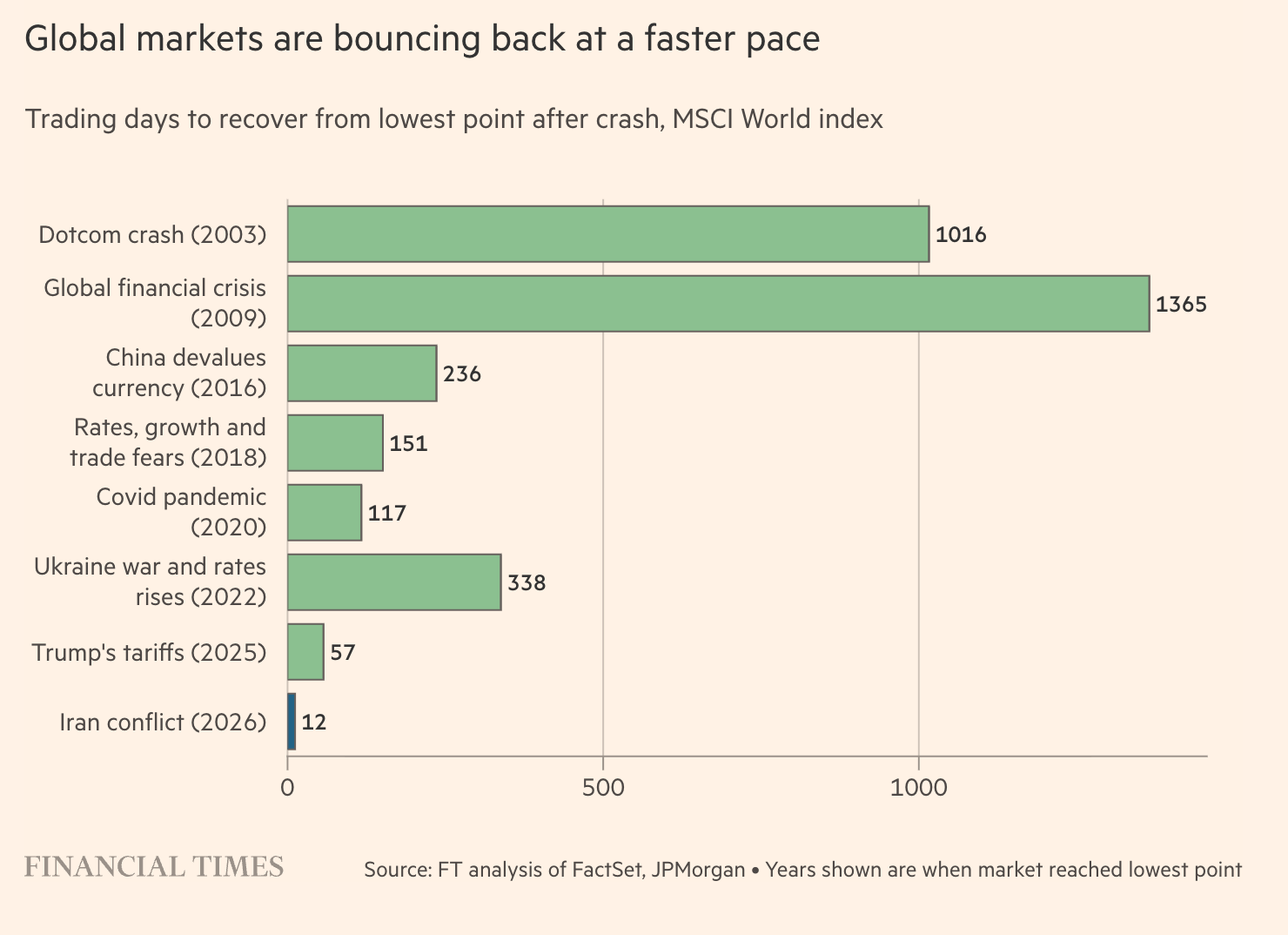

The FT’s chart analysis shows how unusual the current rebound is. The MSCI World index recovered from its low point after the Iran conflict in 12 trading days. After Russia’s full-scale invasion of Ukraine and the 2022 rate shock, the same recovery took 338 trading days. After Covid, it took 117 trading days.

That does not mean geopolitical risk has disappeared. It means the index has recovered faster than the underlying economic damage has cleared.

6) The market’s current answer

At the moment, the market appears to believe that Iran is an oil and inflation risk, but not yet a full global shock. Ukraine remains a major European and fiscal burden, but it is not currently breaking U.S. corporate earnings. AI-related earnings are strong. The U.S. economy remains resilient. Liquidity is still supportive.

That assessment may prove wrong.

But it is not irrational.

Markets can look calm when the world is not calm because markets are comparing forces. Today, AI earnings and U.S. resilience are still stronger than the priced economic damage from Ukraine and Iran.

If the oil channel becomes persistent, if shipping routes are disrupted for longer, if inflation expectations move again, or if escalation changes the policy outlook, that balance can shift.

Our view

The old saying about buying when cannons fire contains one useful lesson: Do not confuse fear with analysis. The weaker version of the saying turns war into a trading slogan. That is too crude.

The better version asks a colder question: Which economic channel has changed?

For investors, the relevant channels are:

energy

inflation

rates

trade

sanctions

defence

reconstruction

confidence.

Our current reading: energy and inflation are the channels to watch most closely. Trade and sanctions are slow-burn risks. Reconstruction is real, but later. Defence remains structurally supported, though not every defence stock benefits automatically.

For the rest of the year, we would expect more sector dispersion than index panic: AI and chips can keep carrying the index, while energy-sensitive, logistics-heavy and consumer-facing businesses feel more pressure underneath.

For founders and CEOs, the same logic applies. The question is not whether the world feels unstable. It does. The question is whether the instability changes costs, customers, suppliers, financing or timing.

Markets may keep rising while wars remain unresolved.

That does not mean the wars do not matter. It means the market has not yet found a transmission channel strong enough to dominate the story.

B O X

For paid readers

‘Pulse’ is where we unpack what is moving.

’Backstage’ is where we turn similar shifts into leadership briefs, decision tools, and operating questions for founders, CEOs and boards.

If you want the practical layer behind essays like this, join Backstage.

🎚️🎚️🎚️🎚️ Producer’s Note

The market is not calm because the world is calm. It is calm because, for now, earnings and AI are louder than oil and war.

That can hold.

Until the channel changes.

StudioAlpha Capital is a Delaware-structured pre-seed venture fund backing AI-native B2B software startups at day zero. Legal counsel: Cooley LLP. Fund administration: AngelList.

Sources

https://en.wikipedia.org/wiki/Norman_Angell