In high school, I had a history teacher who didn’t like me. My grades were bad. He also had a chouchou - same essays, better grades. Since then, I’ve had a mild allergy to historians explaining the world.

Last week in Davos, Yuval Noah Harari explained AI to the world.1

AI is not just another tool. It is an agent. It can learn, decide, invent - and manipulate.

He asked whether AI can think. Whether it can lie. Whether it might soon deserve legal personhood.

However, Harari’s “AI is an agent” framing is kind a shortcut. It compresses a complex stack - infrastructure, compute, models, tooling, constraints, humans-in-the-loop, incentives, guardrails - into one spooky word: agent.

What he didn’t talk about is the one system where agents already act, decide, coordinate, and break things at scale:

Finance.

So let’s skip the moral lecture and look at the plumbing.

What happens when agents don’t just generate words - but move money, settle trades, trigger margin calls, or route payments across systems that must stay correct even when things fail?

What happens when the most conservative machine we’ve ever built meets software that thrives on speed?

Loading...

To answer that, we need to step back. Not to predict the future - but to understand the machine agents are about to touch.

Because the financial system didn’t evolve in a straight line. It evolved through loops.

Those loops explain why finance looks the way it does today; and why every new wave of technology runs into the same hidden constraints.

We’ve seen this loop before. Three times.

And each time, the outcome surprised the people who thought they understood the system.

1. How the Financial system really works (without the banking fog 😶🌫️)

The global financial system is basically two machines:

Capital markets (equities + bonds): where ownership and funding move.

The dollar system: the operating currency of global finance (trade, reserves, funding, risk).

On both machines, the US is the center of gravity.

Pic. Generated by ChatGPT based on this source / friendly reminder: “EU” here is an aggregate, not one market. Europe remains fragmented across countries; unlike the US or UK single market.

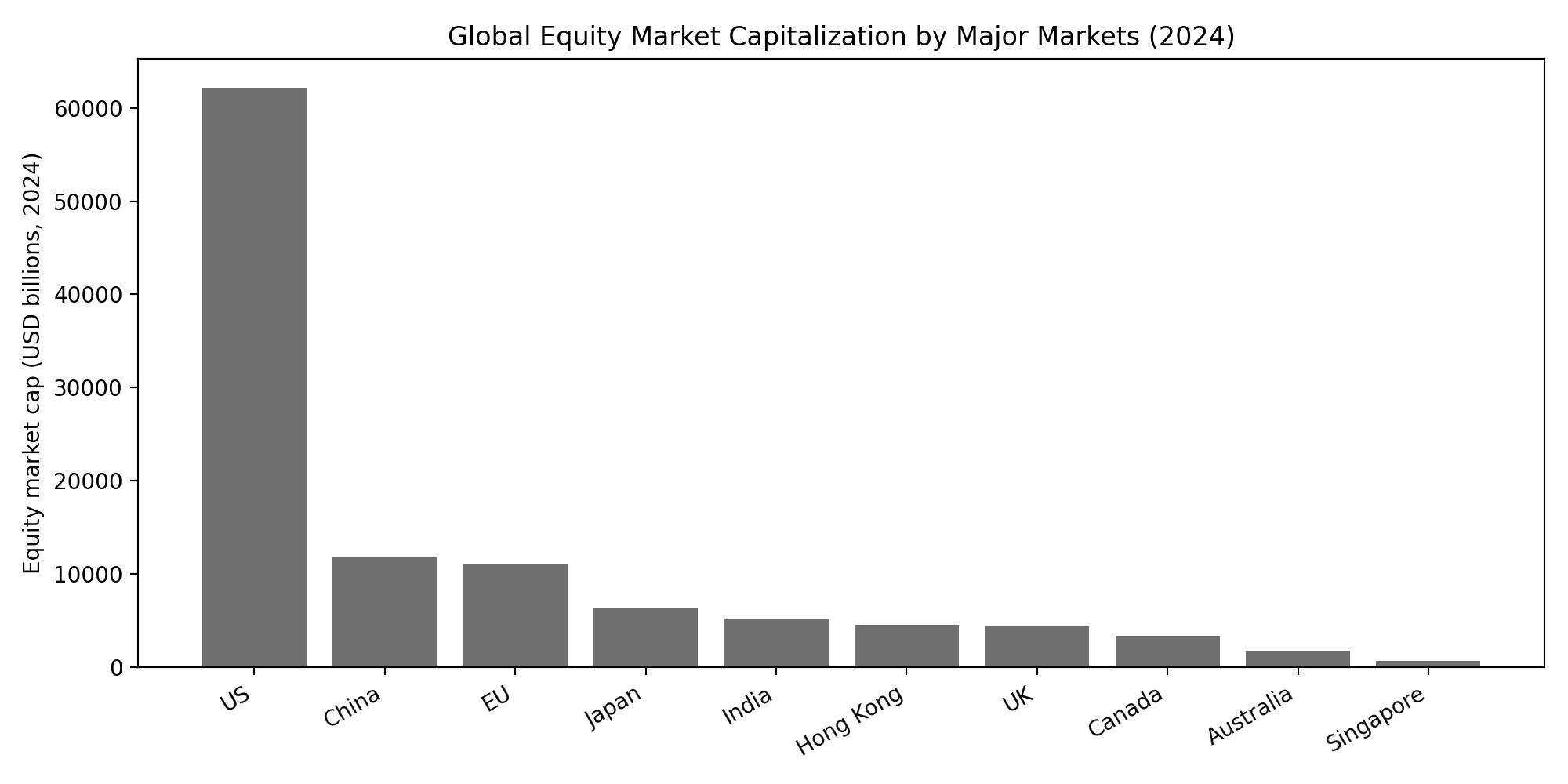

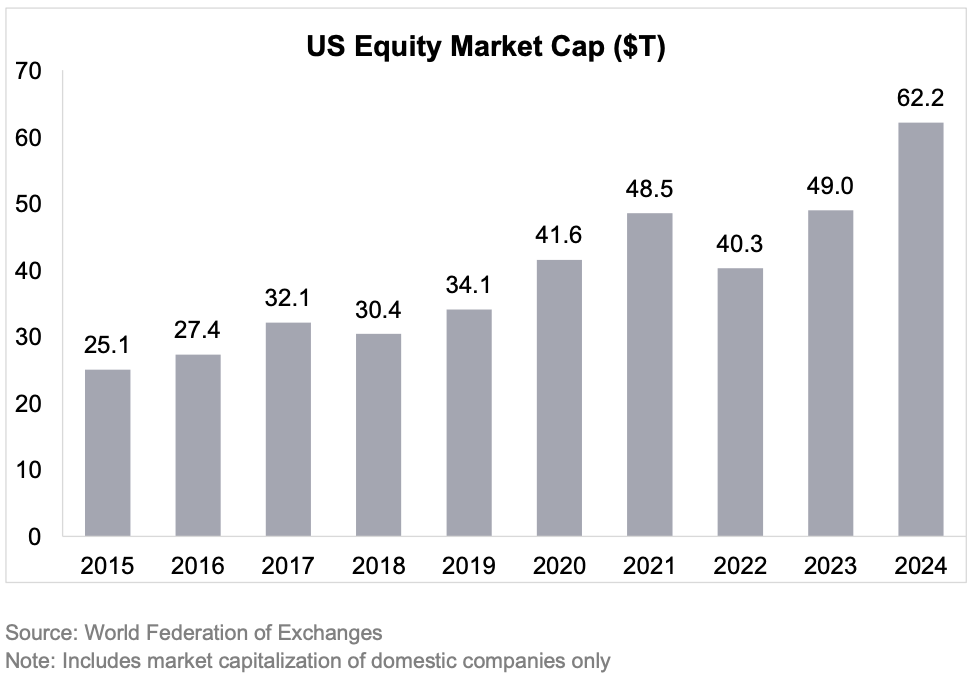

In global equities, the US represents ~49.1% of world equity market cap: about $62.2T out of $126.7T (FY2024).

In global fixed income, the US represents ~40.1% of global securities outstanding: about $58.2T out of $145.1T (FY2024).

In central bank reserves (allocated), the US dollar is still the dominant currency, around mid-50% share in recent IMF COFER data.2

Top 10 “markets” by stock market size (2024)

This table is directly from the SIFMA Fact Book (source: World Federation of Exchanges). Values are USD billions, year-end 2024.3

US — 62,185.7

China — 11,755.8

EU — 11,055.7 (aggregate of 27 countries)

Japan — 6,310.7

India — 5,131.4

Hong Kong — 4,549.7

UK — 4,399.4

Canada — 3,374.5

Australia — 1,737.1

Singapore — 637.6

Even if your product is “global”, in practice US market structure, US rails, and US rules shape a big chunk of the world’s financial plumbing and it is growing.

Pic. One practical implication for founders (face reality / our mantra 🧘🏿♀️): if you build fintech outside the US, you’re not avoiding the US league - you’re postponing it. The moment you show traction, you’ll compete against a US startup (or a US-backed one) that’s trained on deeper capital markets and a single large home market. And while “Europe” looks big on charts, it’s still fragmented in reality: French retail buys mostly French, Germans mostly German, distribution and regulation are national, and liquidity is split. That fragmentation is a tax on speed. So for fintech, starting in the US is not a branding move. It’s a competitive strategy.

So yes - we’ll focus on the US, because it sets the default for a big part of global finance. Now let’s strip away the brand names and look at the system. The financial system does two things:

Move dollars (payments)

Move ownership (securities: stocks, bonds, funds)

If you understand distributed systems, this is familiar: multiple networks, different guarantees, and a lot of coordination to keep everyone on the same state.

Part A - Moving dollars: different “pipes” for different jobs

Think of US payments like transportation. Not one road - many options. In payments, the US uses different rails depending on what you optimize for: cost, speed, and certainty.

ACH = the “batch system”: ACH powers payroll, rent, bills, subscriptions. It processes transfers in batches.4 Example: Your salary shows up later because the system is designed as scheduled batch processing: collect many transfers → process together → deliver. It’s efficient for high volume and low urgency.

Fedwire = “pay more, get certainty”: Fedwire is the high-value rail. It’s real-time gross settlement and, once processed, it is final and irrevocable.56 Example: House closing. Money must arrive now, with no ambiguity. That’s wire territory.7

FedNow = “instant lane”: FedNow is the Fed’s instant payments service (24/7/365), live since July 2023.8 Example: You need to pay a contractor on a Sunday night. You don’t want “tomorrow.” You want “now.”.9

Pic. 🛩️ Get rich quick? Invent the bank. The Medici Bank’s mark in the 15th century - the original “verified” badge. Banking started as trust + documentation. Not apps. (source)

The key concept: fast ≠ final: People confuse:

fast = you see it quickly in your app

final = the transaction is committed in a way that’s legally/operationally hard to unwind

If you’re an engineer: UI success vs committed state. That’s why Fedwire’s “final and irrevocable” language matters.10

And it’s also why building “agent-driven finance” isn’t just a chatbot. Your agent will interact with different rails and must handle different outcomes:

pending

rejected

returned

flagged for review

completed but disputed

That messy reality is where real value sits.

Part B - Moving ownership: buying a stock isn’t “done” when you click Buy

When you buy a stock, you feel like it’s one action. In reality, it’s a process:

the trade happens now

settlement happens later

cash and ownership must be exchanged and reconciled (has it to be reconciled because every software has bugs? > see the deep dive and blockchains role in this footnote11 )

multiple parties must agree on the same state

US markets moved to T+1 settlement effective May 28, 2024.12

Plain meaning: The system reduced the time window to finish the back-end work. Less time means:

The financial system is a trust machine that keeps one promise:

Everyone agrees on the same state.

Who owns what. Who owes what. What is final. What must be reviewed. Who is accountable when something breaks.

That’s the foundation. Now we can talk about agents without hand-waving.

Loop 1: When trust became leverage

Merchants & early banking

Pic. The Medici family transformed Florence from a merchant republic into a cultural and financial powerhouse. (source)

When people talk about “the history of banking,” they usually mean a timeline. That’s misleading. Banking doesn’t evolve linearly. It runs in loops.14

The same pattern has repeated itself three times at scale - with different technology and institutions, but the same underlying logic. Here is Loop 1.

Long before central banks, regulations, or balance-sheet ratios. The system runs almost entirely on reputation.

Trust: merchants, families, city-states

Leverage: deposits get lent out

Growth: trade networks scale

Panic: defaults, runs, war losses

Regulation: reputation and social enforcement

Innovation: paper instruments (not yet money), bookkeeping

New leverage: even larger trade networks

Economic historians like Fernand Braudel describe early banking as a social system - built on trust, reputation, and merchant networks long before formal regulation existed.15

Key takeaway: Banking starts as a social technology before it becomes a financial one.

2. Why the system still feels slow (even though it’s already software)

“Finance is slow because banks run on 30-year-old technology” is a tempting diagnosis - and sometimes true. But even with modern tech, finance would still be slow in many places because it’s distributed, regulated, and designed to stay correct under failure. (See footnote 10.)

Pic. Why banking is slow 🐌: Finance before “APIs” - humans routing everything manually (ca. 1922). Now replace the operators with exception queues and reconciliation teams. Same movie, new cast. (source)

The real bottleneck is coordination, not compute

This is not one system. It’s a network of:

banks

brokers

exchanges

clearing houses

custodians

regulators

internal systems that don’t naturally match

So the hard problem is not “processing power.” It’s: how do we keep everyone in sync?

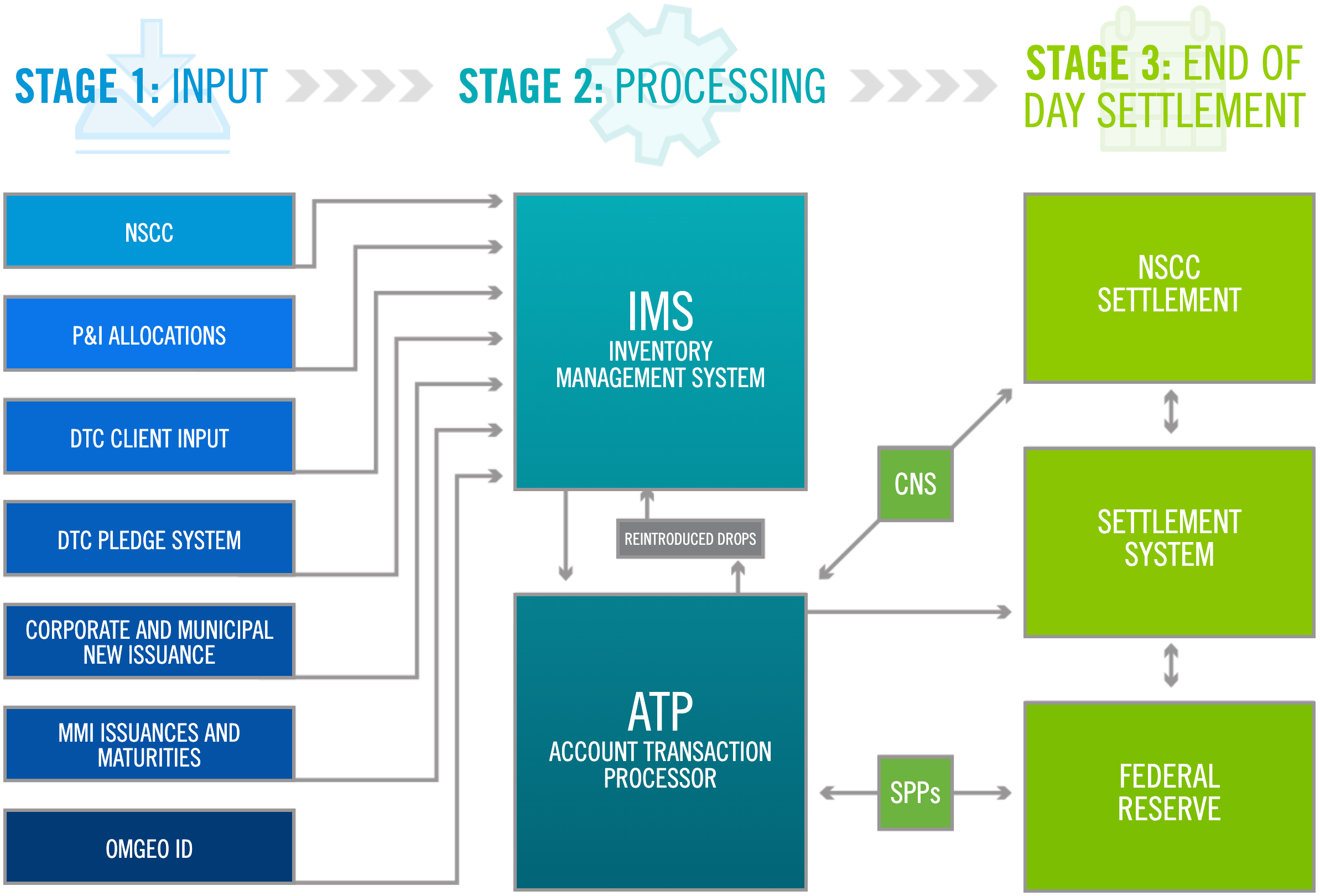

Pic. DTCC’s settlement map. Every box is a different system with its own data and rules. The hard part isn’t compute — it’s keeping all of these systems consistent and handling the exceptions. (Source: DTCC “Understanding the settlement process”; each box is clickable for details.)

👷🏽♀️ Where humans still sit:

Reconciliation: do both sides see the same state?

Exceptions: what if they don’t? (returns, rejects, missing info, mismatched records)

Compliance sign-off: is it allowed? do we have evidence? who is responsible?

Escalation: when it’s ambiguous, a human must own the risk

Even if most transactions are straight-through, the exception tail is where time and cost explode.

Evidence that “plumbing change” is hard: Treasury market clearing reform

A good example of how serious and slow infrastructure change is: the SEC adopted rules to expand central clearing in US Treasury cash and repo markets.16

Pic. Spaghetti 🍝: Payments and settlement work like highway interchanges: many ramps, many rules, many ways to end up in the wrong lane. Agents help by routing and monitoring-boring, but valuable. (source)

Again, this isn’t a UI refresh. It’s a redesign of workflows, responsibilities, and risk management across many market participants.17

Why this matters for agents

Agents won’t magically make the system “instant.”

🤖 But they can reduce the human coordination cost by doing the boring but critical work:

monitor flows across systems

detect mismatches early

route exceptions to the right queue

prepare audit evidence

enforce policy consistently

orchestrate actions across rails without humans babysitting every step

So when we talk about “AI agents in finance,” the first wave is not robots replacing bankers.

It’s agents replacing parts of the coordination layer that still runs on manual workflows and exception queues. Yes, banks are also cutting jobs, but it is more uneven than tech. See explanation in the footnote.18

When people think about “modern banking,” they often think about institutions. But this loop is really about scale.

Nation states, industrialization, and mass credit turn banking into critical infrastructure.

This is the loop where leverage stops being local - and becomes systemic.

Trust: national banks, state backing

Leverage: fractional reserve banking

Growth: railroads, factories, corporations

Panic: bank runs, market crashes, depressions

Regulation: central banks, lender of last resort

Innovation: bond markets, corporate finance

New leverage: larger balance sheets, national credit systems

Economic historians like Charles Kindleberger19 show that financial crises in the industrial era follow a recurring pattern: credit expansion, speculative excess, panic, and institutional response.

Key takeaway: Banking becomes the engine of industrial growth - and a source of systemic risk.

3. Where AI agents actually fit (and where they don’t) - and why this becomes disruptive in 3-5 years

Let’s be precise: in regulated finance, agents won’t win by being “smart.” They win by reducing coordination cost - the human work required to keep many systems consistent, compliant, and correct.

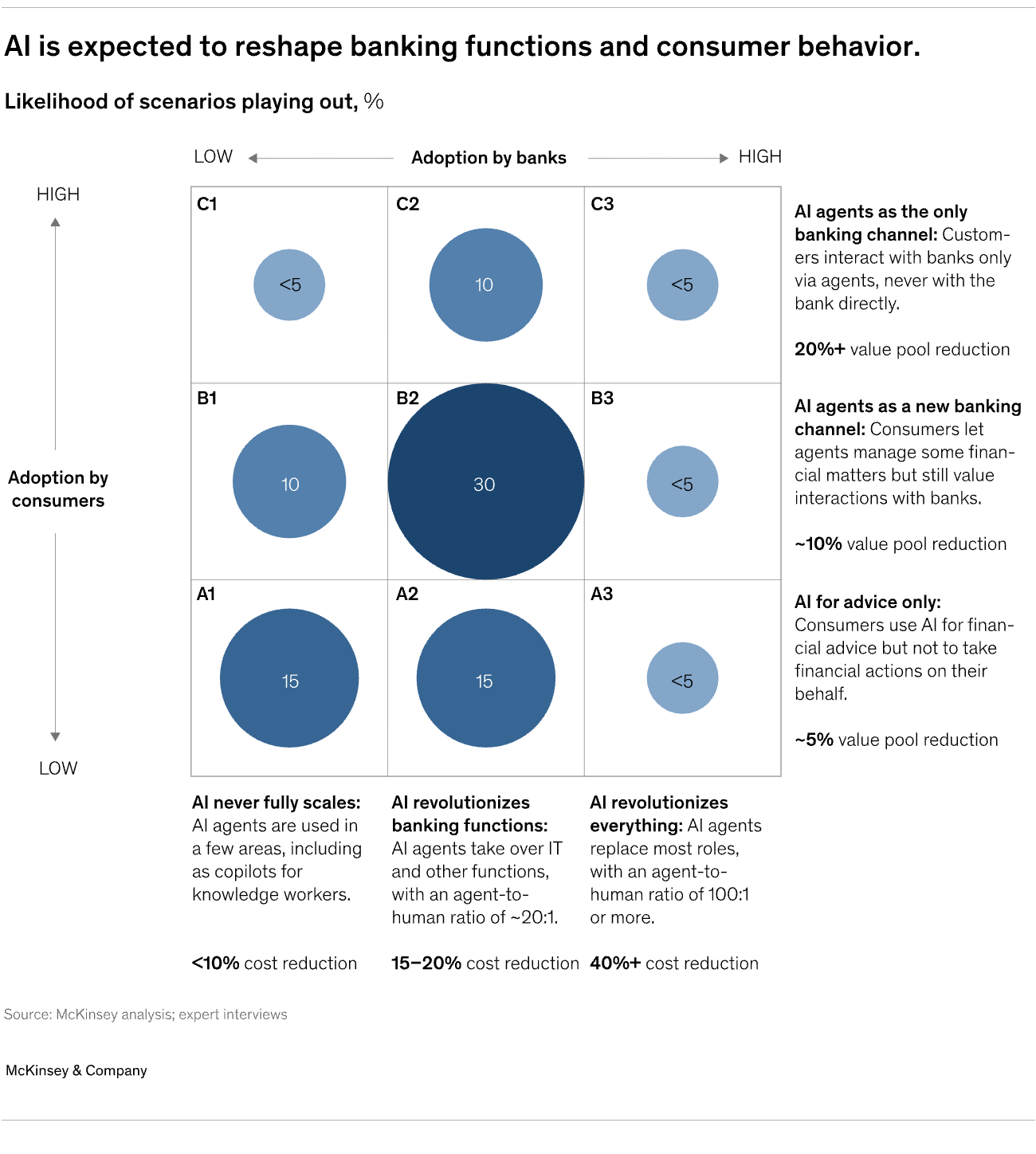

McKinsey’s “agentic era” framing is useful here: banks need productivity, and agentic AI can unlock big efficiency gains - but it can also trigger bigger disruptions if slow movers don’t adapt.20

The constraint most people miss: finance must stay correct under failure

Finance isn’t a single computer. It’s many computers plus regulation plus accountability. That means “the model decided” is not an acceptable answer.

The US supervisory mindset is clear: models that influence decisions require governance, validation, monitoring, and controls (see SR 11-7).21

And the system-level view is just as strict: authorities warn AI can amplify vulnerabilities via opacity, correlated behavior, vendor concentration/third-party dependency, cyber risks, and governance gaps (see FSB: Artificial intelligence in finance).22

So the first viable agent model in banking is not autonomy. It’s: Policy-bounded execution with an audit trail.

The forcing functions (why the next 5–10 years matter even without a new rail)

Here is the balanced reality: the rails won’t flip overnight, but the system is already under pressure from structural changes.

Payments remain multi-rail: The US will not “switch to one payment system.” It adds capability while legacy rails keep running:

FedNow provides instant payments capability (24/7/365) and is live.23

Fedwire remains the high-value certainty rail with finality.25

Post-trade is already compressed: US securities moved to T+1 settlement effective May 28, 2024.26

Core market plumbing is being redesigned: The SEC adopted rules to expand central clearing in US Treasury cash and repo markets.27

Translation: even if regulation stays conservative, the system is tightening deadlines and increasing standardization. That increases coordination work unless you automate it.

How “disruption” happens even if the rails don’t change overnight

Here’s the balanced view that avoids both extremes (“nothing changes” vs “everything flips next year”):

Workflow economics can change quickly once coordination work gets automated at scale.

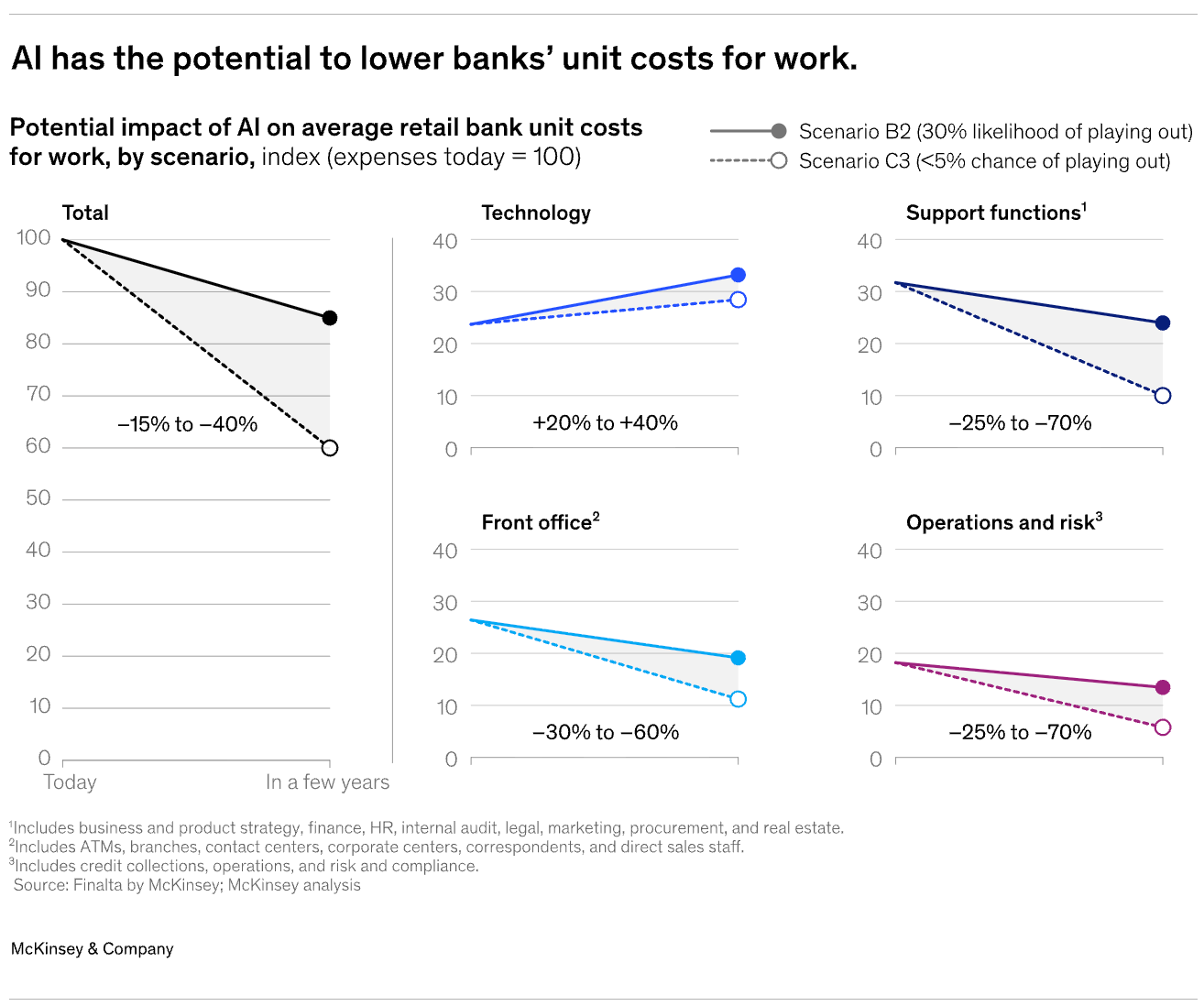

McKinsey puts numbers behind that: AI could drive gross reductions up to ~70% in some cost categories, with net 15–20% cost-base reduction after higher technology costs.28

They also expect a breakout agentic business model to emerge in 3–5 years, creating a tipping point.29

Notice what this implies: you don’t need a new payment rail to get disruption. You can get disruption from cost structure, operational speed, and customer expectations.

Operator reality check: Schuyler Weiss (Light Frame) - an ex-banker building the plumbing

Schuyler Weiss is the CEO and founder of Light Frame (since Jan 2024), a StudioAlpha portfolio company building next-generation systems for private banks and wealth managers. Before that he co-founded and led Alpian (Jan 2020–Dec 2023), a Swiss digital private bank incubated by REYL; Alpian publicly announced in September 2023 that he stepped down as CEO after leading the build-out to major milestones, including securing a FINMA banking license. His career is a classic “finance + platform” path: IBM financial-services consulting in New York, then Morgan Stanley in product/digital roles, then back to Geneva as Chief Digital Officer at REYL where the Alpian journey started; he also holds an MBA from IMD. That mix matters: he’s not theorizing about how banks adopt tech - he’s lived the constraints (regulation, risk, integration) and now builds infrastructure designed to survive them.

Pic. Schuyler Weiss - banker hair, confirmed.

He shared a useful operator’s framework after a discussion with a senior Swiss banking executive:

• Short term (0–2 years): Experimentation. The tech is not ready for banks yet. It’s still too inconsistent - and too costly - to trust with critical workloads. First movers run pilots, learn, and define guardrails.

• Medium term (2–7 years): Productivity. Banks deploy AI in select parts of the stack and drive real but limited efficiency across front and back office. Differentiation (and ROI) goes to those who execute well.

• Long term (7+ years): Intelligence. AI systems are broadly deployed, managing most workflows autonomously and reliably. Some banks re-architect around this future - and the gap to slow movers becomes material. Bankers still matter; AI boosts their efficacy. A portion of clients adopts AI-driven offerings. Both models coexist, but the mix shifts over time.30

His bottom line is pragmatic: banks are complex by design and must be cautious - but given the capital and pace behind AI, it will likely be the most transformative technology of his generation, and there’s a rare window to act early.

Loop 3: When software accelerated the loop

Modern & digital finance

Pic. Lehman Brothers Files For Bankruptcy Protection (source)

If Loop 2 was about scale, Loop 3 is about speed.

Computers, global markets, and financial engineering compress the loop. What once took decades now happens in years — sometimes months.

The logic stays the same. The system just runs faster.

Trust: insured deposits, market infrastructure

Leverage: securitization, wholesale funding

Growth: globalized capital markets

Panic: 2008 financial crisis

Regulation: capital, liquidity, stress tests

Innovation: fintech, APIs, digital rails

New leverage: automation, programmability, speed

Economists like Hyman Minsky argued long before 2008 that stability itself breeds instability — because success encourages ever more leverage.

Key takeaway: Technology didn’t break the banking loop. It compressed it.

Where agents land first (high ROI, low drama)

Agents will first be deployed where three things are true:

the work is repetitive and coordination-heavy

actions can be constrained by policy

logs and evidence have direct value

That clusters into three practical buckets:

1) Ops + exception handling (the real cost center) Most financial workflows are automated in the happy path. The money and time disappear in the unhappy path: rejects, missing data, mismatches, failed settlement, compliance holds, “pending review” queues.

Agents can do the boring part reliably:

classify the issue

fetch missing context

route to the right queue

propose a resolution path

keep an evidence trail

This is not “AI does decisions.” It’s “AI removes manual babysitting.”

2) Compliance evidence (proving you did the right thing) A lot of compliance pain is not the rule itself. It’s proving you followed the rule after the fact.

Agents can continuously assemble:

logs

timestamps

policy references

“why did we do X?” explanations

evidence bundles for audits

This aligns with the governance expectation behind SR 11-7: documentation, monitoring, controls.31

3) Orchestration across systems (the distributed state problem) Because the US is multi-rail (ACH32, Fedwire33, instant34), coordination work is real even when everything is “digital.” Agents can act like middleware:

choose the correct execution path under policy

monitor state across systems

retry safely

escalate with context when ambiguity appears

This is where agents reduce coordination cost without changing the underlying rails.

Where agents should not be trusted first (yet)

To stay honest:

unbounded discretionary decision-making (large transfers, credit decisions, changing risk limits on the fly)

autonomy without auditability (no clear reason, no logs, no stop conditions)

designs that increase correlated behavior at scale - a key systemic concern highlighted by the FSB (FSB AI in finance).35

Takeaway

The first wave of “agents in finance” is not robots replacing bankers.

It’s agents replacing parts of the coordination layer that still runs on manual workflows, exception queues, and evidence gathering - while operating inside clear policy boxes.

That sounds boring. It isn’t. It’s the part of finance that actually costs time and money.

4. The radical scenario: programmable settlement + agents as the operating layer

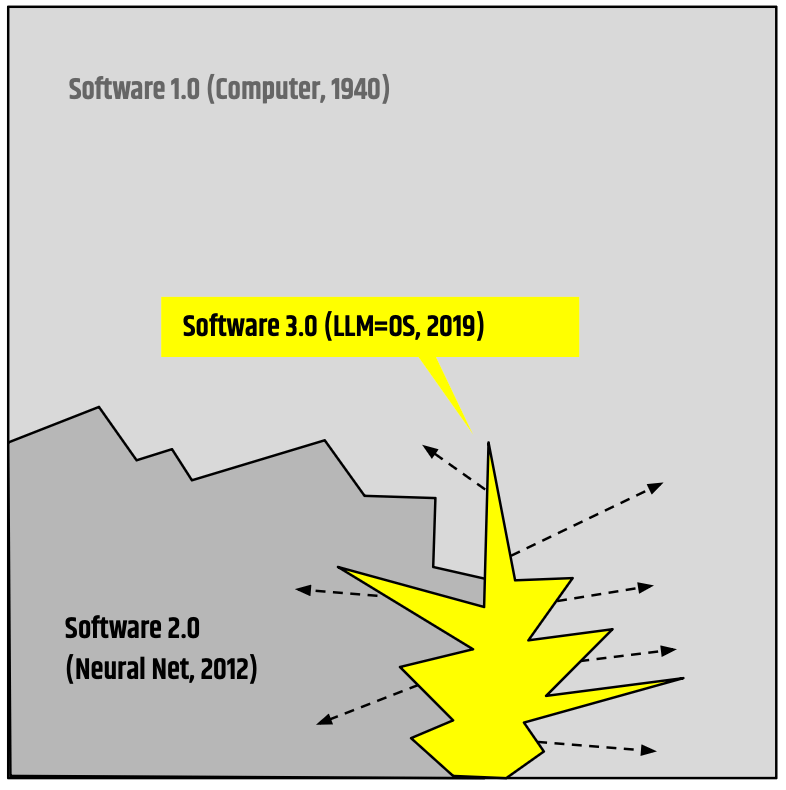

This radical scenario is not guaranteed. And it won’t happen because retail crypto is loud. Assumption: LLM is the new operating system and all software will be rebuilt over the next 10 years - not only banking systems.36

Pic. Friendly reminder: LLM as the new Operating System (Andrej Karpathy)

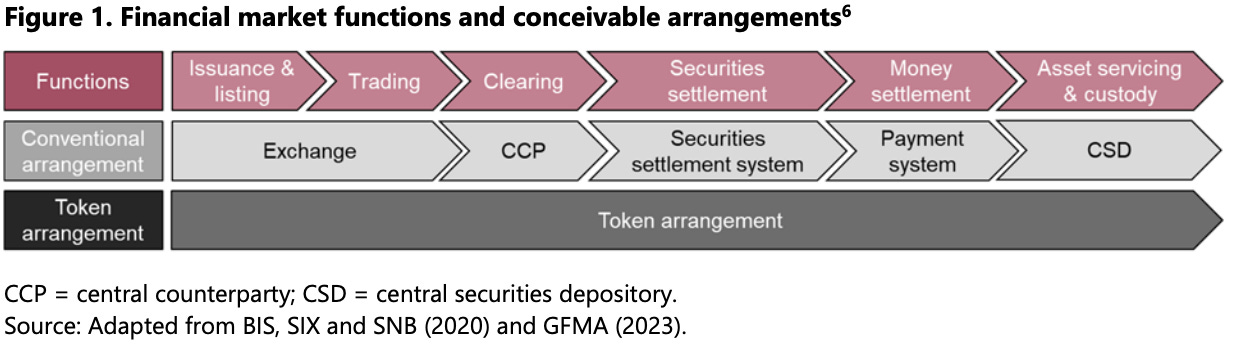

If it happens, it happens because regulated wholesale infrastructure moves from “message passing between institutions” toward shared programmable settlement.

What “programmable settlement” means (plain language)

Today, a lot of finance still works like distributed databases without a shared commit log:

In the radical scenario, parts of this become closer to shared state:

transactions are represented as state transitions on a common platform

the cash leg and the asset leg can settle together (“atomic” style)

constraints and controls become executable logic

audit evidence is produced by default

This is not “banks disappear.” It’s “settlement becomes more like software with shared state.”

Why this is not a fantasy: Tier-1 institutional signals exist

The Bank for International Settlements (BIS) and CPMI published a major report on tokenisation and programmable platforms - explicitly discussing how token arrangements can change market structure and what governance/risk management is required.37

And BIS Innovation Hub’s Project Agorá is explicitly exploring a multi-currency unified ledger for wholesale cross-border payments.38

BIS even put out a press release arguing that a tokenised unified ledger could lay foundations for the next phase of the monetary/financial system - again, this is institutional, not retail hype.39

Translation: the serious tokenisation path is moving through wholesale settlement and market infrastructure, not memecoins.

Where agents come in (and why they become the operating layer)

If settlement becomes more programmable, the bottleneck shifts.

Today the bottleneck is coordination work:

exceptions

reconciliation and state mismatches

manual compliance evidence

“who approves what” workflows

In a programmable-settlement world, the bottleneck becomes:

defining policies precisely

enforcing them consistently

operating workflows continuously

producing audit and compliance evidence in real time

That’s where agents can evolve from “helpers” into an operating layer:

Agents become the interface between:

policy (what is allowed)

execution (what happens)

evidence (why it happened)

Builder preview: Bill Sun and the agentic exchange model

This is where Bill is useful: he shows what “agent-native finance” looks like when someone actually builds it.

Pic. Bill Sun — formal attire. In reality, he’s usually in builder mode.

Bill Sun sits at the intersection of frontier AI and real-world market execution. He is the co-founder of AIUSD / Generative Alpha (agentic trading + “agentic money” infrastructure) and a co-founder of PIN AI (personal AI platform). He’s a Stanford Math PhD with experience spanning early AI research at Google Brain and quantitative roles at major trading firms, and he frames AIUSD as building “AI-native money infrastructure” for agents. We met at our StudioAlpha JAM in San Francisco, and in our interview (Jan 12, 2026) he explains the “analyst + execution trader” pattern and his longer-term “financial OS” vision.

His deck makes the same point visually. The following pic “One AI to rule all blockchains” shows the before/after:

Before: users jump between multiple wallets, multiple DEXs, and bridge platforms - with manual routing, friction, and bridge/security risk.

Now: the user writes one instruction (“swap X on chain A to Y on chain B”), and the agent orchestrates the multi-step execution end-to-end.

That is exactly our thesis in miniature: agents reduce coordination cost by doing the orchestration work humans currently do manually.

Bill’s longer-term “north star” (from our interview) goes further: a “financial OS” where agents manage ongoing monitoring and execution and eventually interact economically with other agents.

We keep this honest:

Bill’s model is a builder preview of agent-native execution

it is not “institutional reality” yet

the institutional path is BIS/Agorá + governed adoption

US regulation path (what actually matters for builders like Bill)

For builders like Bill, the near-term “radical scenario” isn’t only BIS-style infrastructure. It’s the US legal path that decides what can scale:

Stablecoins: the GENIUS Act created a federal framework for payment stablecoins in the US, pushing the market toward regulated issuance and clearer rules for who can issue and under what requirements.40

Market structure: the CLARITY Act is designed to define regulatory lanes—giving the CFTC a central role for “digital commodities” while preserving parts of SEC authority for token fundraising and securities-like activity.41

Yield: the big open question is whether a “stablecoin” stays a simple payment instrument or turns into something closer to a yield product. Regulators globally treat stablecoin-related yield as a risk amplifier, and approaches differ.42

Tokenized stocks: the path to tokenizing real-world assets is not “crypto gets a free pass.” Even SEC leadership voices have stressed that tokenized securities are still securities—the wrapper doesn’t change the legal nature.43 And the market is actively pushing the regulated route: legacy incumbents like ICE/NYSE are developing platforms for 24/7 trading and on-chain settlement of tokenized securities (pending approvals).44

Translation: the “radical” future is less about memecoins and more about whether the US successfully industrializes the legal rails for (1) stablecoins, (2) market structure, and (3) tokenized securities.

The hard constraints (why this stays conditional)

This only scales if the governance and systemic-risk requirements are met:

1) Model / automation governance must be industrial-grade The core mindset is already codified in US banking supervision: governance, validation, monitoring, controls (SR 11-7) .45

2) Systemic AI risks must be actively engineered down FSB is explicit about AI-related vulnerabilities in the financial sector (opacity, concentration, correlated behaviors, cyber/governance gaps). Use the working FSB report.46

3) Tokenisation must move beyond pilots (selectively) Project Agorá is explicitly framed as testing desirability/feasibility/viability - i.e., it’s still a journey.47

So the radical scenario won’t arrive as “one big migration.” It arrives corridor-by-corridor, asset-by-asset, with governance baked in.

That maps cleanly onto the radical scenario:

the UI becomes intent

execution becomes policy-bounded automation

settlement becomes more programmable

agents coordinate actions and compliance continuously

But we keep it honest: builder ambition is not institutional reality. The institutional reality is BIS/Agorá direction + governance constraints (SR 11-7 + FSB).

Takeaway

Balanced scenario: agents become the glue inside today’s fragmented rails and workflows.

Radical scenario: parts of settlement become programmable shared state, and agents evolve from glue into the operating layer for policy + execution + audit.

But it only happens if:

tokenisation moves into production in specific wholesale domains (BIS/Agorá)

If you only take one idea from this post, take this:

In the next 3-5 years, AI agents won’t replace the financial system. They’ll replace chunks of the human coordination layer inside it.

That’s where the time and money still burn: exceptions, reconciliation work, evidence gathering, and cross-system orchestration - all under tight governance constraints.48

For founders

Don’t pitch “AI in finance.” Pitch governed execution. If your agent can’t show what it did, why it did it, and what would have stopped it, you’re not selling into regulated workflows - you’re selling a demo.

For incumbents

The threat isn’t a better model. It’s a competitor who industrializes workflows faster: fewer exceptions, faster resolution, cleaner evidence trails. That can be disruptive even if rails evolve slowly.

For investors

Most “AI finance” is UX. The deeper wedge is infrastructure: workflow automation, compliance evidence, and orchestration across a multi-rail system.49

And one last reality check: if you’re building fintech outside the US, you’re not avoiding the US league - you’re postponing it.

For Harari

You handle the philosophy. Builders will handle the failure modes. ☮️

One-line takeaway: Agents don’t make finance “instant.” They make it run with less human coordination, and that shift will reshape competition.

🎚️🎚️🎚️🎚️ Producer’s Note

Harlem, NYC: A$AP’s new album out Jan 16, 2026. I like experiments 🧪 - Let’s be experimental with AI Agents, too. An album for the history? - Ask an historian ;]

“Reconciling”: It’s not mainly because “banks make mistakes.” It’s because the system is distributed.

When you buy a stock, there isn’t one shared database where “truth” is written once. There are multiple ledgers that must end up consistent:

your broker’s records

your broker’s clearing firm

the central securities depository / settlement system

the buyer/seller sides

cash accounts at banks / payment rails

So reconciliation exists for three reasons:

Many ledgers, one truth Each party keeps its own books. After the trade, they need to confirm they all reflect the same trade details and positions. That’s reconciliation.

Timing gaps Trade execution happens now, settlement happens later (even at T+1). In between, positions and cash move through processes. Reconciliation checks that the expected moves actually happened.

Exceptions happen (this is where “mistakes” come in) Yes: wrong account details, missing reference data, corporate actions, failed funding, cut-off times, tech glitches, etc. Reconciliation is how the system detects and fixes mismatches before they become legal fights.

“Reconciliation exists because finance isn’t one computer. It’s many computers that must agree.”

Is blockchain a fix? - Yes — in theory, that’s one of the main promises.

Reconciliation exists because we have many ledgers and they have to converge to one truth. A blockchain (or any shared ledger) tries to reduce that by making multiple parties write to one shared state.

What blockchain can solve (theoretical upside)

Single source of truth: instead of Broker A and Broker B each updating their own database and later reconciling, they both update a shared ledger.

Atomic settlement (in principle): cash leg + asset leg can settle together on the same platform (or coordinated platforms), reducing “fails.”

Audit trail by default: every state change is logged and verifiable.

This is basically the “programmable settlement / unified ledger” idea we referenced with BIS/Agorá.

What it does not magically solve (practical reality)

Identity + permissioning: regulated finance needs known parties and access controls.

Legal finality: the law has to treat the ledger’s state as definitive ownership.

Privacy: markets can’t expose everyone’s positions and trades publicly.

Performance + resilience requirements: big markets need insane throughput, uptime, and controlled failure modes.

Integration: even if settlement is on a shared ledger, you still need to integrate with the rest of the system (banks, reporting, risk, custody).

So the honest conclusion:

Blockchain can reduce reconciliationwhere you can move multiple parties onto a shared ledger with the right legal + governance wrapper.

But it’s not a flip-the-switch solution for the entire financial system — it’s more realistic in wholesale / specific corridors first.

“Blockchain is a reconciliation minimizer — but only where you can make shared state legally real and operationally governable.”

Charles P. Kindleberger (with Robert Aliber), Manias, Panics, and Crashes - especially the early chapters where they lay out a stylized sequence: speculation/credit expansion → financial distress → crisis/panic/crash, plus policy response.

Yes — banks are also cutting jobs, but it’s more uneven than tech.

What’s happening in banking right now

Cost-cutting + restructuring is real, especially in retail/commercial banking and in back/middle office functions. Example: Metro Bank is starting another redundancy round (about ~100 roles) as part of its turnaround and shift away from low-margin retail lending. (Reuters)

Big-bank restructurings continue. Citi is cutting about ~1,000 jobs (and has signaled headcount reductions continue into 2026 as part of its multi-year simplification). (Reuters)

Switzerland/Europe: UBS is still in “Credit Suisse integration mode.” Reuters reported UBS may cut up to ~10,000 further roles by 2027 (mostly via attrition, early retirement, internal moves, etc.). (Reuters)

But it’s not a straight “Amazon-style” story

In tech, you see huge, centralized layoffs (Amazon just announced ~16,000 corporate job cuts). (Reuters)

In banking, it’s more like continuous trimming + reorgs, plus selective hiring in areas that are hot (e.g., parts of investment banking / trading when markets are strong). (Reuters)

My take

Banking layoffs are absolutely happening, but the driver is usually structural (integration, branch/retail pressure, efficiency, regulation, automation) rather than one giant “reset” like in Big Tech.

: Posters & Prints")

")

.jpg")

{kind=link}

.jpg){kind=link}

{kind=link}