A year ago, “AI bubble” was a reasonable shorthand.

Today it’s mostly a distraction.

Because the debate has moved from valuation to capability.

Last week Anthropic announced Claude Code Security1 — an agentic tool that can scan real codebases, surface high-severity vulnerabilities, and suggest patches for human review.2

On Monday, cybersecurity stocks didn’t wait for a macro narrative. They repriced immediately. And on Tuesday, software stocks got a brief reprieve — the S&P software index bounced — but it’s still down hard year-to-date.3

Loading...

*Just to be clear: YES means “we’ll look back and laugh.” NO means “we’ll look back and say: that was the moment the control point moved from humans clicking software to agents doing work.” Welcome to the show — you’re betting the white-collar Western world is about to see its job map rewritten.

That’s what markets do when a new capability threatens an existing profit pool.

So what are we actually watching?

A temporary scare around tech capex?

A rotation out of the Magnificent 7?

Or something deeper: the early economics of AI becoming a real production layer — the kind that rewires categories, compresses margins, and creates new winners before the index even moves?

This post is a map for that moment.

We’ll look at why the S&P can sit still while the market underneath behaves like a regime shift. We’ll look at Europe’s inflows and ask if this is a real comeback. And we’ll look at what happens when AI stops being a feature and becomes infrastructure — and which business models get repriced first when it does.

1) The Illusion of Calm

If you look only at the index, the year feels boring. The S&P 500 is roughly flat.

But the market under the index is anything but calm.

The FT reports that more than one-fifth of S&P 500 stocks have already moved up or down by more than 20% this year, even while the index treads water. It also notes the gap between large single-stock moves and subdued index performance is the highest since 2009, with Citadel Securities calling dispersion “extreme.”4

That one stat tells you more than a week of punditry.

This isn’t “sell America” panic.

It’s repricing.

In transitions, the index can look calm because the winners and losers cancel each other out. Meanwhile, the internal market becomes a battlefield: AI helps some business models, threatens others, and forces many to retool fast. The more credible your “AI leverage,” the more investors forgive cost and capex. The more exposed you are to AI disruption, the quicker your multiple compresses.That is exactly why the “AI bubble” narrative is too simple. A bubble implies broad, uniform over-excitement. What we’re seeing is uneven, model-by-model repricing. That’s not a bubble popping. It’s a system reallocating.

If you want the technical label, the right word is dispersion — not volatility. Dispersion captures the spread of returns across stocks even when index-level moves are muted.5

Now add the human label the FT used: FOBO — fear of becoming obsolete. That’s what’s driving the “shoot first, ask questions later” behavior in software. Or: selling software stocks without thinking … panic-mode.

And add the market-structure amplifier: the FT describes “pod shops” (multi-strategy hedge funds) as increasingly price-setting here — teams with low tolerance for drawdowns, trigger-happy on headlines.6

So yes, you’ll see violent rotations. And no, not all of them will be durable.

But the underlying thing is real: AI capability is moving fast enough to reprice categories.

Here’s what dispersion looks like in real life: one product announcement and an entire software category reprices in a day. When Claude Code Security hit the tape, the market wasn’t reacting to “macro.” It was reacting to a new capability that potentially shifts value from monitoring to automated repair.7

One more detail from Tuesday’s bounce matters: investors didn’t just sell software — they rotated into “tangible asset” sectors. Utilities, energy, and materials have been winners in 2026. One strategist called them “Halo” stocks: heavy asset, low obsolescence.8

Pic. Break the S&P 500 into sectors and the “calm” disappears. (source)

That’s not “physical beats digital.”

It’s “capital-light businesses feel more disruptable when AI becomes a production layer.”

Zoom out for a second: this is exactly how big market shifts often start — the index looks quiet while leadership rotates underneath.

Box: Why the Index Can Look Flat When Something Big Starts

Most long-term investors are told to keep it simple: buy the S&P 500, keep adding, don’t overthink it. Even Warren Buffett famously instructed that 90% should go into a low-cost S&P 500 index fund.9

That advice is still directionally right for “normal” life investing.

But here’s the trap: during big platform shifts, the index can look calm while the market underneath is in a knife fight.

The early 2000s were the classic example. From January 2000 through December 2009, the S&P 500 delivered roughly -0.95% annualized — the “lost decade.”10

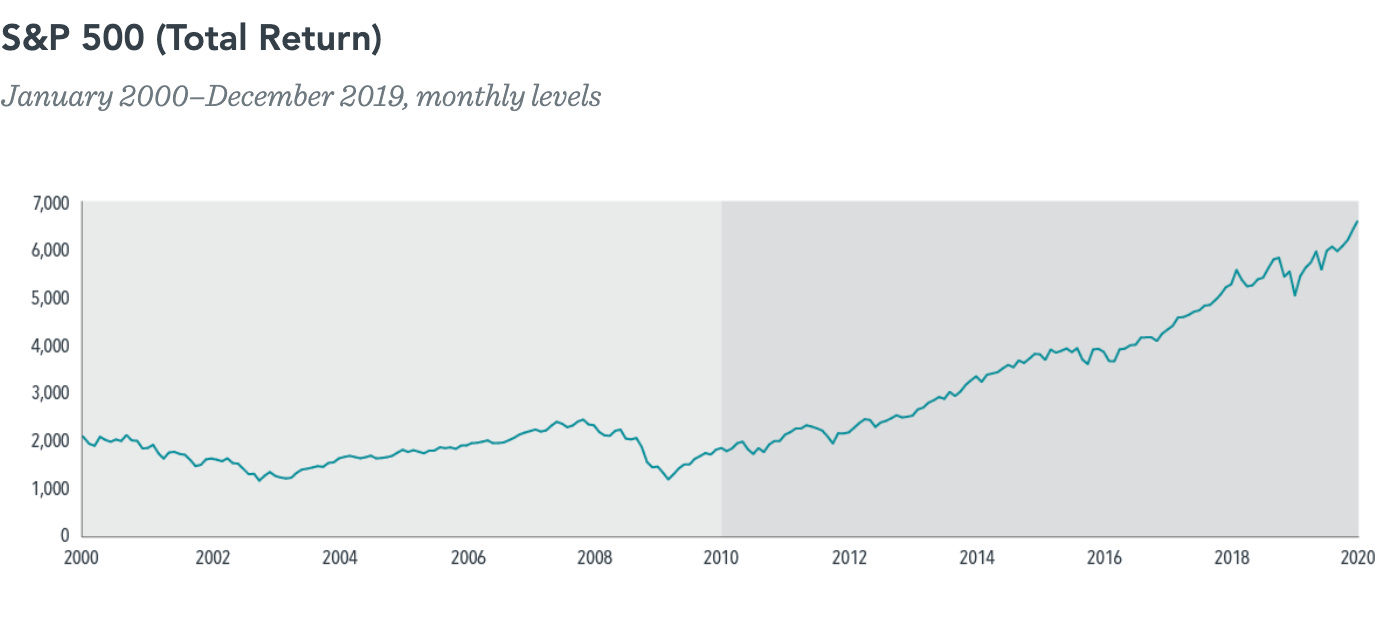

Pic. When S&P500 was not a good idea - The lost decade 2000-2010 (source)

The economy didn’t stand still in that decade. Leadership just rotated hard — dotcom collapsed, housing boomed, commodities ran, then the financial system cracked.

That’s why dispersion matters. Dispersion measures how far stocks (and sectors) spread apart even when the index itself barely moves.11

So when you see “index flat + extreme dispersion + violent sector rotation,” it’s not proof of a supercycle — but it can be an early market signal that the system is being repriced.12

(And yes: dollar-cost averaging is still a legit behavior tool — Vanguard’s own work shows why people use it, even if lump-sum wins more often historically.)13

And if this really is a platform shift, the next question isn’t what pundits say — it’s what the builders are doing with real money.

2) While Everyone Debates, The Builders Write Checks

Now the part that breaks the meme.

If AI were “just hype,” you’d expect the builders to pause. Capex would slow. The infrastructure wave would cool. Boards would pull back and wait for clarity.

Instead, the largest companies on earth are doing the opposite.

Even if you don’t want to rely on aggregated press figures, you can anchor the behavior directly in primary company guidance.

Meta’s investor materials include capex guidance in the $115–135bn range for 2026.14

Alphabet’s investor materials include capex guidance in the $175–185bn range for 2026.15

Microsoft’s FY2026 Q2 earnings call materials cite $37.5bn quarterly capex and explicitly note that roughly two thirds is going into short-lived assets like GPUs and CPUs — i.e., the compute build-out.16

And Amazon’s 2026 capex expectations being around $200bn has been widely reported as part of the market’s “capex anxiety” story this year.17

Box: The Dotcom Fibre Glut vs. AI Factories

The last time markets saw a “build-out,” it ended painfully: the late-90s telecom boom laid huge amounts of fibre that stayed dark for years. In 2002, the WSJ cited TeleGeography estimating that only ~2.7% of installed fibre was actually in use.18

Prices collapsed accordingly — bandwidth costs fell >90% in the years after the bust.19

AI looks different on one key dimension: the constraint isn’t demand — it’s inputs.

Power: AI data centres are already running into grid limits and reliability warnings.20

Chips: demand for leading AI GPUs has repeatedly exceeded supply due to manufacturing bottlenecks.21

That doesn’t mean “no bubble” is possible. It means the base case isn’t “empty fibre in the ground.” The base case is “scarce power + scarce compute” — and the system reprices around whoever controls those bottlenecks first.22

This is why the capex is rational: each new agentic feature doesn’t just “add value” — it can reprice entire software categories overnight, as security just learned.

Now step back and look at what this really means.

This is an infrastructure sprint financed by private balance sheets. We are watching industrial policy executed by corporations: data centers, energy procurement, chips, networking, cooling, and a new layer of software built on top.

Yes, there can be overvaluation. Yes, there can be bad startups, bad money, and bad bets. But bubbles don’t normally come with this kind of sustained, system-level capital formation.

Production shifts do.

In the sense of completeness: OpenAI’s valuation …

Pic. Valuation OpenAI vs. Anthropic (Series G at$380B post-money, Feb 2026 (source, source2)

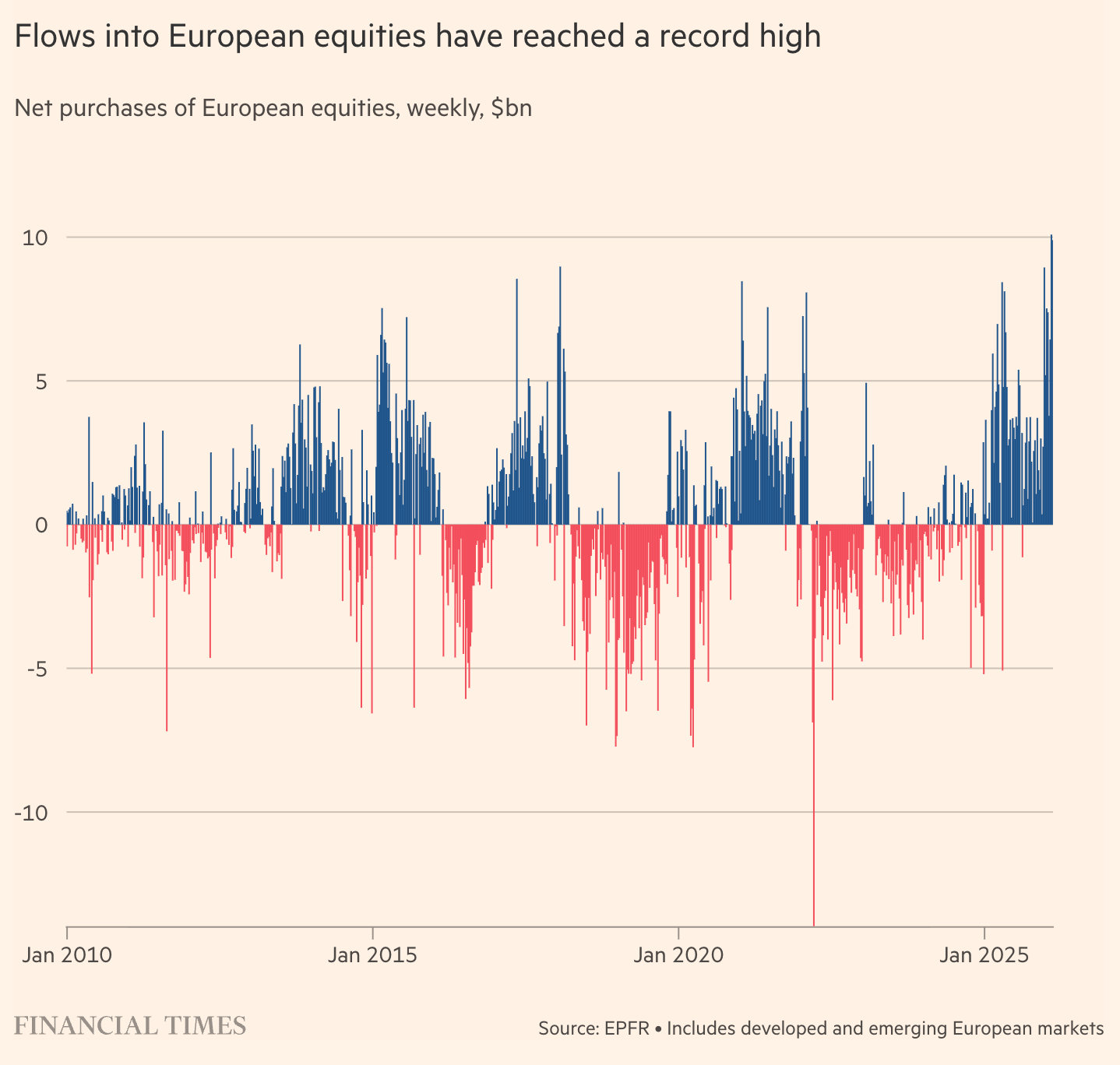

3) Europe Is a Hedge, Not a Challenger

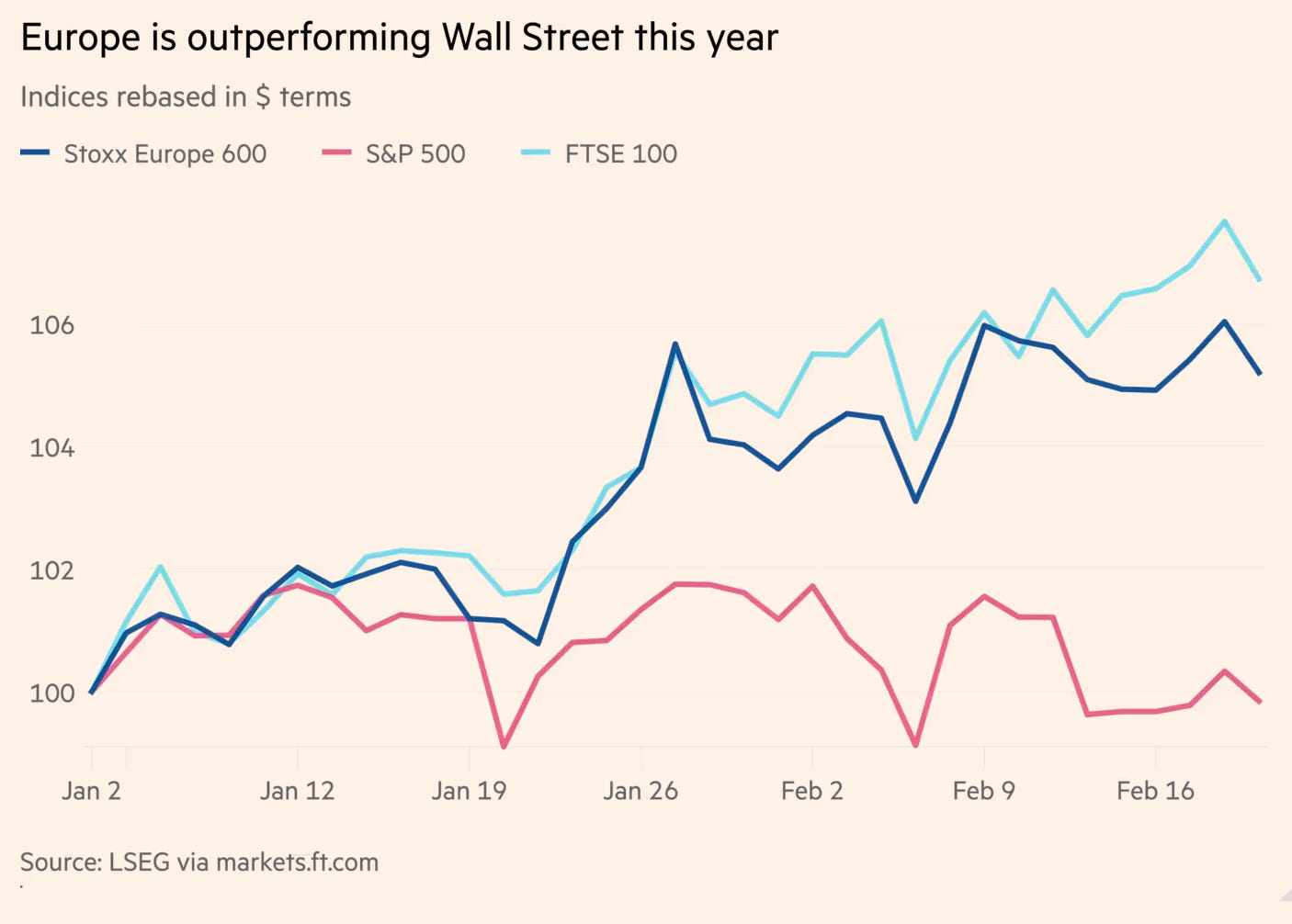

Europe is getting real inflows right now. No debate. The FT reports European equities are on track for their highest ever monthly inflows in February, with two consecutive record weekly flows of about $10bn, based on EPFR data.23

And this links directly to what’s happening in the US: part of the rotation has been into tangible-asset sectors — utilities, energy, materials — and Europe simply has more of that “old economy” exposure.24

But we should be honest about what investors are actually buying when they buy “Europe” in this moment.

They are not buying European AI leadership. They are buying diversification away from US tech concentration — and a valuation gap. The same FT piece says it directly: investors want different exposure, and Europe “has less tech.” It also cites the valuation spread: the Stoxx Europe 600 around 18x earnings versus roughly 27x for the S&P 500 (per LSEG, as quoted by FT).25

A hedge against Magnificent 7 dominance. A hedge against AI concentration. A hedge against mega-cap capex anxiety.

That hedge can be smart tactically.

But a hedge is not a challenger.

Europe does not currently sit at the center of the AI platform stack. It doesn’t have the same hyperscaler cluster controlling global cloud distribution. It doesn’t have the same concentration of compute, capital, and frontier model leadership at scale.

This is not trash talk. It’s structure.

So when capital rotates into Europe, it tends to rotate into sectors outside the AI platform core — banks, industrials, defense, energy, cyclicals. These sectors can do very well in a “rotation year,” especially when the US index is dominated by a handful of mega-cap names.

But let’s not confuse tactical positioning with structural technological catch-up.

Here’s the deeper issue, and this is the part Europe keeps avoiding.

Europe’s problem is not talent. Europe has exceptional engineers. The issue is incentives and participation. As described in our blog las week: Europe still has lower retail participation in capital markets compared with the US — which reduces the political and cultural flywheel for pro-growth, pro-equity outcomes. The EU Council notes that in 2021 only about 17% of EU household assets were held in financial securities (shares, bonds, funds, etc.), compared with about 63% in the US.26

(Source: statista 2024)

When fewer citizens participate in equity upside, societies become more suspicious of equity outcomes. That shows up in narrative, in policy posture, and in risk tolerance. And in platform shifts, risk tolerance is not a vibe — it’s a competitive input.

So yes: Europe can outperform tactically for long stretches. It can rotate, re-rate, and catch a wave of inflows.

But if AI is a production layer, the uncomfortable reality is that hedging the shift is not the same as participating in it.

You don’t beat a production shift by avoiding it. Let’s say the quiet part out loud: no risk, no upside. If Europe keeps treating equity outcomes as suspicious, venture as “casino,” and platform builders as something to regulate first and celebrate later, then we shouldn’t be shocked when the next wave is won elsewhere — again. We already watched it with the internet, mobile, and large parts of cloud. AI won’t be different just because Europeans hope to “win the second half.” In a capacity race, you don’t win the second half. You win by showing up in the first.

4) Bubble vs Production System

Every major technological transition in history contained bubbles.

🚂 Railroads created speculation and collapse — and still reorganized logistics. 💡 Electricity created winners and wipeouts — and still rewired productivity. 🛜 The internet created the dotcom crash — and still became the operating system of modern life.

So the “bubble” framing is not useless. It’s just incomplete:

A production shift can contain bubbles. A bubble does not negate a production shift.

Two Different Worlds (and people keep mixing them)

AI as “Bubble” AI as “Production System”

---------------- -------------------------

Valuation story Capacity story

Sentiment & multiples Capex & infrastructure

Rotations & narratives Build-out & adoption

Short-term mean reversion Long-term compounding

“Which stocks are expensive?” “Who is building the system?”

And that last row is the new part investors are suddenly waking up to:

AI agents can change where the control point sits.

The FT’s “adapt or die” piece frames the $64,000 question as disintermediation: do AI agents step between the user and existing software systems — turning old software into back-end plumbing while value moves to an agent layer?27

This is why the market is struggling: two things can be true at the same time.

Incumbents have real moats: distribution, integration, trust, switching costs.

Agents can still disaggregate value: systems of record remain, but the “system of work” moves elsewhere.

The shift from cloud to SaaS ended up being great for many incumbents. This AI shift could also expand markets — but not necessarily with the same winners, and not necessarily with the same business models.28

That’s why the “digital to physical” narrative becomes a category error.

The physical build-out is not competing with AI. It is being forced by AI.

Data centers are physical. Chips are physical. Power is physical. Cooling is physical. Grid reliability is physical. Yes — that was already true last year. And in the 90s. And basically since we discovered electricity :] The point isn’t that AI touched the physical world. It’s that it’s now pulling on these constraints at industrial scale. The frontier AI stack is as industrial as it is digital. And yes - software was already digital in the 90s ;]

So when investors say “physical is back,” what they often mean is: the AI build-out is forcing a capex cycle that looks like old-school industry.

That doesn’t make AI smaller.

It makes AI bigger.

It means the AI conversation must move from “cool software” to “capacity race” — and now also: control-point migration.

5) The Real Divide

This is not US vs Europe.

And it’s definitely not digital vs physical.

The real divide is:

AI as a valuation trade. Versus. AI as a capacity race.

When you look through that lens, the “sell America” narrative becomes less convincing and more theatrical.

The FT’s NIIP piece points out that overseas investors bought a net $1.55tn of long-term US assets in 2025 — and uses this to argue fears of capital flight are currently overdone.29

The same article explains why this matters: US equity outperformance has dramatically widened global imbalances, because non-Americans own so much of the US market’s best assets. If the US equity boom reverses sharply, the shock spreads beyond America.

Translation for normal humans:

🇺🇸 The world is already financially tied to US tech leadership.

🌎 If AI compounds through US platforms, global investors benefit.

🥃🥃🥃 If it collapses, the pain isn’t “American.” It’s global.

So the “Europe is safer” narrative is, at best, incomplete. Even if you rotate tactically, the system remains anchored to US AI capacity.

That’s why your blog can be blunt without being emotional:

Europe can hedge. ✍🏼 America is building. 🏗️

In the long run, capacity wins.

What This Means for Founders

Founders don’t get paid for predicting narratives.

They get paid for building inside compounding waves.

So the practical takeaway is not “buy US, sell Europe.” That’s retail finance theater. The practical takeaway is: don’t outsource your thinking to the “AI bubble” meme.

If AI is a production shift, then disruption is not optional. Customers will expect AI-native workflows. Competitors will compress costs with automation. Products will be compared to systems that do the work, not tools that merely assist.

Waiting for consensus is a strategy for losing.

Build. Integrate. Ship.

And if you are building in Europe, you need an extra dose of realism. You are operating inside a system that still has lower equity participation, lower tolerance for power-law outcomes, and more regulatory friction — while the center of capacity build-out sits elsewhere 🌁.

That doesn’t mean you can’t win.

It means you must win by execution and distribution, not by hoping Europe “wins the second half.”

Production shifts reward builders. Not commentators.

🎚️🎚️🎚️🎚️ Producer’s Note

Hectics time at the financial markets? Cool song to relax.

Brent Faiyaz is one of the defining voices in modern alternative R&B — independent, low-key, and very intentional about staying outside the traditional label machine. Born in Columbia, Maryland (1995), he broke through with GoldLink’s “Crew” and has built a cult-level following since.