Incumbents Kill Startups. Sometimes.

A real-world playbook of copying, bundling, buying — and the patterns that decide who dies, who pivots, and who exits.

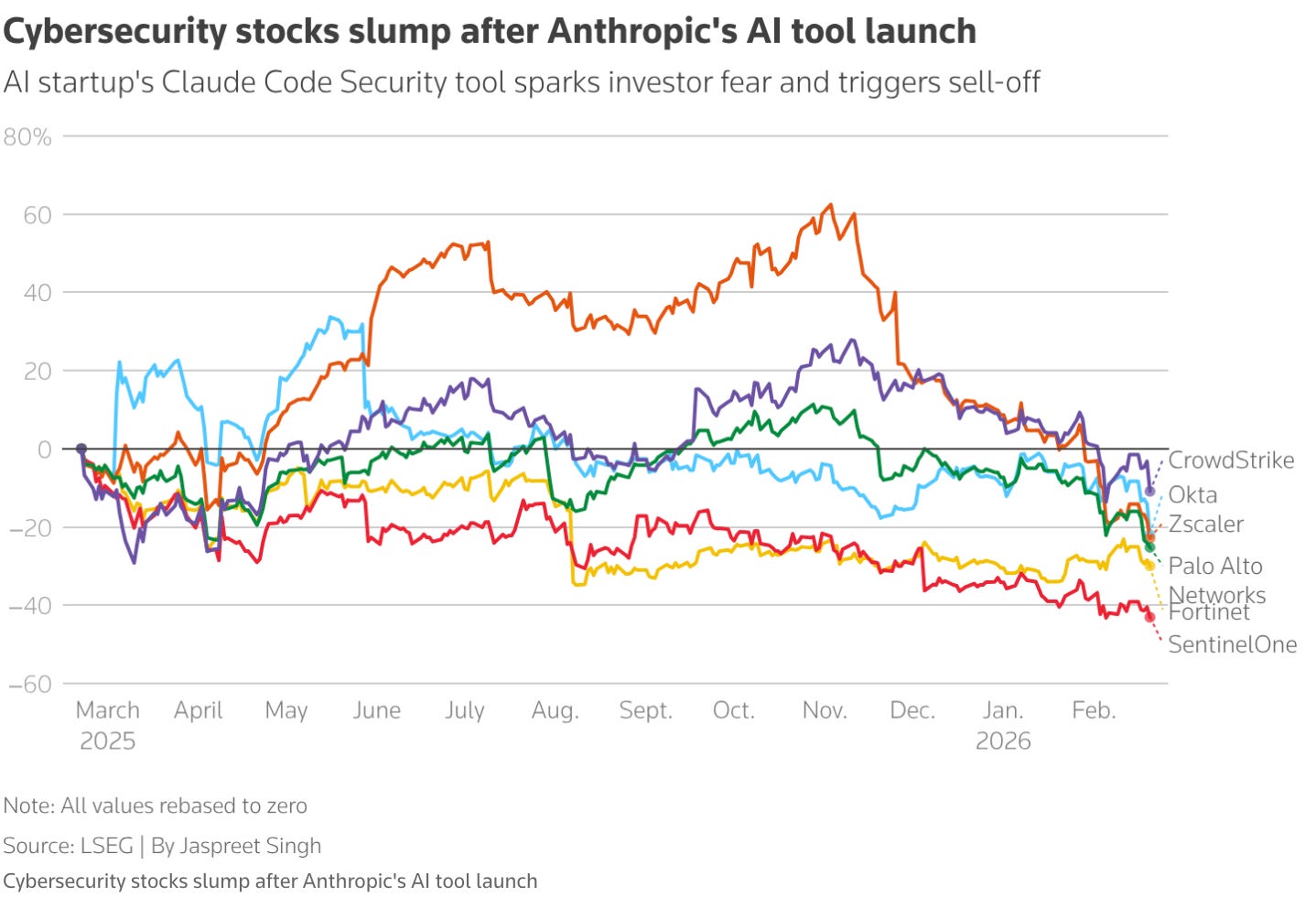

Last week, the market gave us a reminder of who owns the “high ground” in software.

After Anthropic announced a security-focused AI capability, several public cybersecurity names sold off (CrowdStrike, Datadog, Zscaler, etc.) — not because they missed earnings, but because investors instantly priced in a new reality: the model providers are moving into the application layer.1

And then, one day later, came the second signal — even more revealing: Anthropic softened its own safety commitments, explicitly pointing to competitive pressure. In plain English: “we can’t afford to be the only ones slowing down.”2

Every founder has this thought at 2 a.m.:

“What if we build this thing… and then Google / Microsoft / Apple / OpenAI / Anthropic just ships it as a feature?”

It’s not paranoia. It’s a rational fear — and it has moved up-market. It’s no longer just early-stage teams asking this question. It’s later-stage category leaders, and even AI-native companies building on top of the same platforms that might later compete with them.

In the 90s it was the OS and the browser. In the 2000s it was search and marketplaces. In the 2010s it was mobile and app stores. Now it’s the AI assistant becoming a new “interface layer” — and when the interface layer shifts, entire software categories get repriced.

We’ve seen this movie before. The names change. The mechanics don’t.

So instead of hand-waving it away — or turning it into a moral debate — this post does the boring but useful thing: it breaks down how this actually plays out in the real world. When incumbents copy and kill. When copying backfires. When the startup pivots and wins. When the outcome is an acquisition instead of a war.

Same story every decade. New interface layer. Old powers. Fresh founders.

Part I - The Map

1. Why this topic is back (and why AI changes the stakes)

Before we get into mechanisms and outcomes, it helps to remember: this game has roles.

The classic pattern is old: platforms expand. Microsoft did it. Google did it. Apple did it. And now the AI labs are doing it too.

What’s different this time is speed and surface area.

In the old cycles, “moving downstream” took years. New products had to be coded, shipped, distributed, adopted. Today, model providers can ship a new capability, wrap it in an assistant UI, and distribute it instantly to millions of users already sitting inside their product.

Model providers are no longer “just” infrastructure. They’re actively turning the model layer into an application layer:

OpenAI launched the GPT Store — basically an app marketplace inside ChatGPT.3

Google is building Gemini directly into Workspace apps (Docs, Gmail, Meet, etc.). That’s distribution at the point of work — where habits already live.4

Anthropic pushed “Artifacts” and then “apps inside Claude” — turning the chat UI into a lightweight application runtime.5

This matters because it changes the competitive geometry.

The fear is not “Big Tech copies startups.” That’s old news.

The fear is this:

When ChatGPT / Claude / Gemini become the default front door for knowledge work, they can absorb huge parts of the software stack.

In previous eras, the “interface layer” was the thing users opened first:

Windows and the browser in the 90s

search and marketplaces in the 2000s

mobile and app stores in the 2010s.

Now the AI assistant is becoming that layer — the place where work starts, and increasingly where work happens.

And once the assistant6 becomes the front door, a lot of software stops being something you “open” and becomes something the assistant “calls” in the background.

Instead of opening Jira to write a ticket, you tell the assistant: “Create a ticket, assign it to X, summarize the call notes, set due date Friday.”

Instead of opening a legal drafting tool: “Draft an NDA based on our template, highlight unusual clauses, export to Word.”

Instead of opening a security dashboard: “What’s the riskiest alert this week, what changed, what should we fix first?”

For users, that’s great. It’s less clicking, less searching, more outcomes.

For software companies, it changes everything.

Because if the assistant owns the front door, it can bundle the most common workflows as built-ins. Entire categories risk becoming “just a prompt” or “just a built-in tool.” Not because startups are bad — but because the platform owns distribution and can make a feature feel “free” inside an existing subscription.

That’s the modern version of bundling.

And it’s why LPs ask the question again — not as a philosophical concern, but as a very practical one:

If the platform keeps moving downstream, where can startups still build durable value — and where are they simply building features that will be integrated away?

If you want a modern AI-era example that captures this fear in one clean story: Jasper.

In 2022, Jasper raised $125M at a $1.5B valuation, riding the first wave of LLM-enabled marketing copy.7

Then OpenAI released ChatGPT to the public on November 30, 2022 — and overnight a huge chunk of “AI writing” went from paid product to free-ish default.

It wasn’t even malicious. It was the platform doing what platforms do: integrate the most common use case.

That Jasper moment is the perfect bridge into the first category we need to analyze: when incumbents copy (or bundle) and the startup collapses — not because the team is stupid, but because the product was shaped like a feature.

That’s Chapter A1.

2. The 5 mechanisms incumbents use

People say “they copied us.” That’s not precise enough.

There are five recurring mechanisms incumbents use to win downstream. And each one produces different outcomes.

Mechanism 1 - Bundling / tying (default distribution wins): If you control the OS, the browser, the app store, the enterprise suite — you can ship a feature to millions overnight.

This is the oldest weapon in the book.

Mechanism 2 - Self-preferencing (rank yourself first): If you control a marketplace, a feed, a search engine, a directory — you can put your product at the top and quietly starve others of oxygen.

Mechanism 3 - Platform rule changes (API, policy, permissions): If you depend on the platform, they can change the rules: access, rate limits, permissions, background activity, pricing, store policies.

No drama. Just a “developer update”.

Mechanism 4 - Cross-subsidy / price compression (“free” beats “best”): Incumbents can bundle the feature into an existing contract, price it at zero, and force the market into a margin collapse.

Mechanism 5 - Data advantage (they sit on the workflow): When the incumbent already owns the workflow and telemetry, it can build the feature faster and improve it faster.

This is especially relevant in AI, where feedback loops matter.

3. The outcomes

Here’s the key: the mechanism doesn’t automatically determine the outcome.

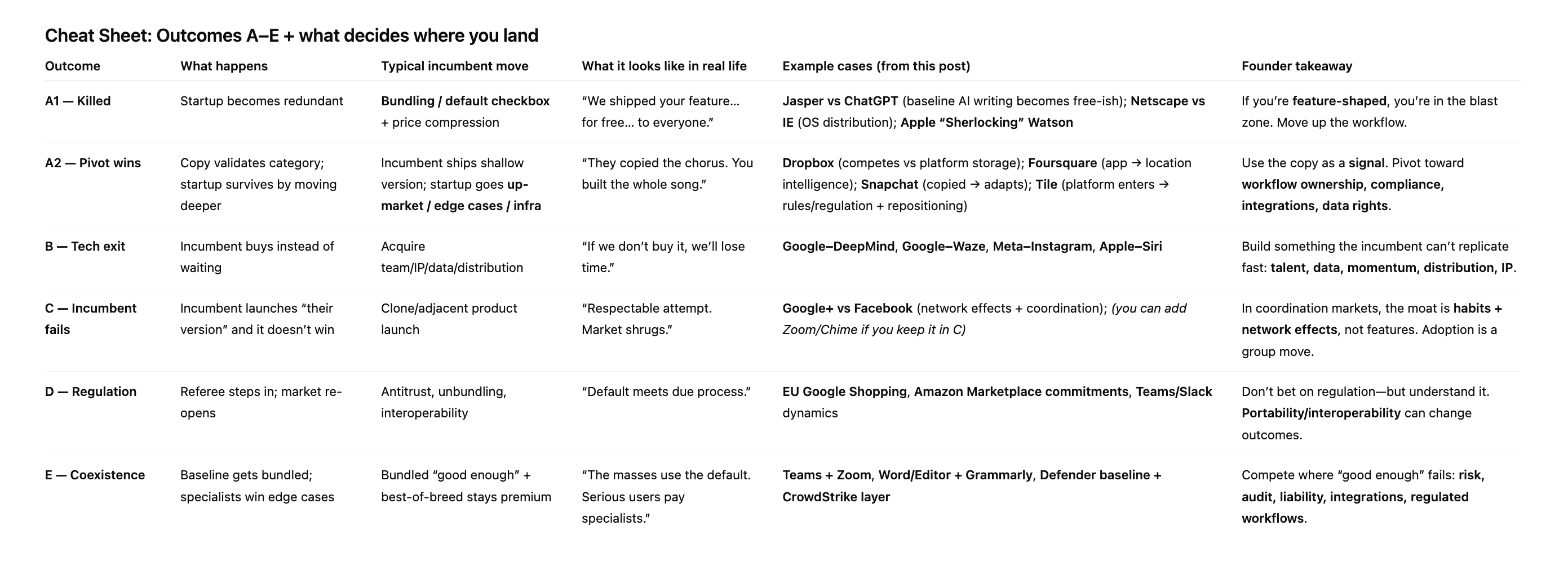

In practice, we see six outcomes:

⛔️ (A1) Copied / bundled → startup collapses

✅ (A2) Copied / bundled → startup pivots and survives (sometimes thrives)

✅ (B) Copied → the incumbent buys it (company or capability)

✅ (C) Copy attempt fails → startup wins anyway

✅ (D) Regulation shifts the game → category re-opens

✅ (E) Coexistence → “good enough” for the mass market, specialists thrive at the edge

Most founders only see A1. That’s why they panic.

But the real world is messy — and the other branches happen constantly.

Part II - The Evidence

4. (A1) Copied / bundled → startup collapses | When incumbents actually kill startups ⛔️

Let’s not sugarcoat it.

Sometimes a platform ships your product as a checkbox and you’re done.

This tends to happen when:

the startup is feature-shaped (not a workflow owner),

switching costs are low,

distribution is controlled by the incumbent,

and the incumbent can ship “good enough”.

Case: Microsoft vs Netscape (bundling + OS leverage)

The Internet Explorer era is the canonical story of tying and distribution power.

The U.S. v. Microsoft findings of fact describe the market dynamics around Windows’ dominance and Microsoft’s conduct around browsers and threats to the OS monopoly.8

You don’t need to argue ideology here. The lesson is mechanical:

If your competitor owns the default distribution layer, product quality alone won’t save you.

Case: “Sherlocking” — Apple shipping your app as a built-in feature

This is so common it has a verb.

Apple shipped Sherlock 3 with functionality that developers argued closely matched Karelia’s Watson, and “being Sherlocked” became a term in the Mac dev world.9

This is A1 in its purest form: a platform feature makes a third-party product economically irrelevant.

Case: GO Corp / PenPoint vs Microsoft (the “early pen computing” war)

GO Computer’s PenPoint is often cited as an early example of platform pressure in a category Microsoft wanted to control.

There’s real case material around GO’s antitrust claims related to Microsoft’s conduct and PenPoint technology.10

Be careful with wording (because history gets mythologized), but the pattern is again mechanical:

When the platform owner decides your category is strategic, they can drag the center of gravity into the platform and starve independent players.

5. (A2) Copied → pivots and survives | When the startup pivots and becomes more successful ✅

Now the part many people miss:

Copying can validate the category.

Bundling can expand the market.

And incumbents often ship a shallow version — which creates room for specialists.

This branch happens when the startup is not a feature, but a workflow owner.

Dropbox: surviving the “OS bundling” era by moving up-market

Dropbox has competed for years against platform providers (Microsoft, Google, Apple). They even spell it out in their own filings: competition, replication risk, and platform dynamics are real.11

Dropbox didn’t win because it was “first”. It survived because it became a broader workflow product, built brand trust, and pushed into enterprise needs that aren’t solved by a checkbox.

Foursquare: from consumer app → location data infrastructure

Foursquare is a classic pivot story: consumer growth slows, the “app” becomes less relevant, and the company shifts to selling location intelligence / data products.12

This is the A2 move: escape the feature trap by moving to a layer the incumbent can’t easily “bundle away.”

Snapchat vs Instagram Stories: copied hard, still alive

Instagram Stories was widely described as a very direct copy of Snapchat’s core format.13

Snap didn’t die. It adapted. That’s the important part.

If your identity is “one feature”, you’re dead.

If your identity is a product ecosystem, audience, or workflow… you can survive a copy.

Tile vs Apple AirTag: platform enters the category, the fight becomes about rules

Tile’s story shows another survival pattern: once the platform competes with you, the battle shifts to platform access, permissions, and fairness — and often becomes regulatory.14

Tile didn’t magically win — but it didn’t vanish overnight either. The “platform competition” dynamic changed the whole category.

6. (B) Copied → Incumbent buys it (company “tech exit” or capability) ✅

Sometimes the platform doesn’t want to wait.

Sometimes the asset is too strategic: team, data, IP, momentum.

So the incumbent buys.

Google ↔ DeepMind

DeepMind is a canonical example of “strategic capability acquisition” in AI.15

Google ↔ Waze

Waze is a clean example of buying a mix of product + community + data.16

Facebook ↔ Instagram

The Instagram acquisition is the textbook “buy what you can’t ignore.”17

Apple ↔ Siri

Apple acquired Siri (the company/app) and integrated it deeply into the OS.18

Sometimes “buy” doesn’t mean acquiring the company. It means the incumbent becomes your customer first — procurement, licensing, co-production. In mission-critical areas (defense, security, regulated enterprise), that’s often how “ownership” starts: prove it works, then the buyer pushes to control supply and integration.19

Key insight: B is often the outcome when the startup has something the incumbent cannot replicate quickly without losing time in a strategic race.

7. (C) Copy attempt fails → startup wins anyway | When incumbents try, but can’t ship the real thing ✅

One mental trap founders fall into is thinking: “If the incumbent ships the same feature, we’re dead.”

Sometimes that’s true (that’s A1). But surprisingly often, it’s not.

Incumbents copy. Incumbents bundle. Incumbents launch “our version of X.”

And then… nothing happens. The startup keeps winning.

Why?

Because copying a feature is easy. Copying the why people choose it is hard.

Three reasons incumbents often fail here:

They ship a compromise, not a product.

The startup is obsessed with one thing. The incumbent is balancing ten internal agendas, legacy users, legal, brand risk, and channel conflict. The result is often “good enough,” but not loved.They’re trapped in their own ecosystem.

Startups win by being the neutral layer: working across platforms, being the best tool for external collaboration, or fitting into messy real-world setups. Incumbents tend to optimize for their own stack first.Network effects and habits are real.

In categories where people coordinate with other people (music, meetings, social), being “built-in” is not enough if the experience isn’t better and the network isn’t there.

Let’s make it concrete.

Case 1: Spotify vs Apple / Amazon / Google — bundling didn’t dethrone the specialist

If bundling were the whole game, Spotify should have been crushed a long time ago.

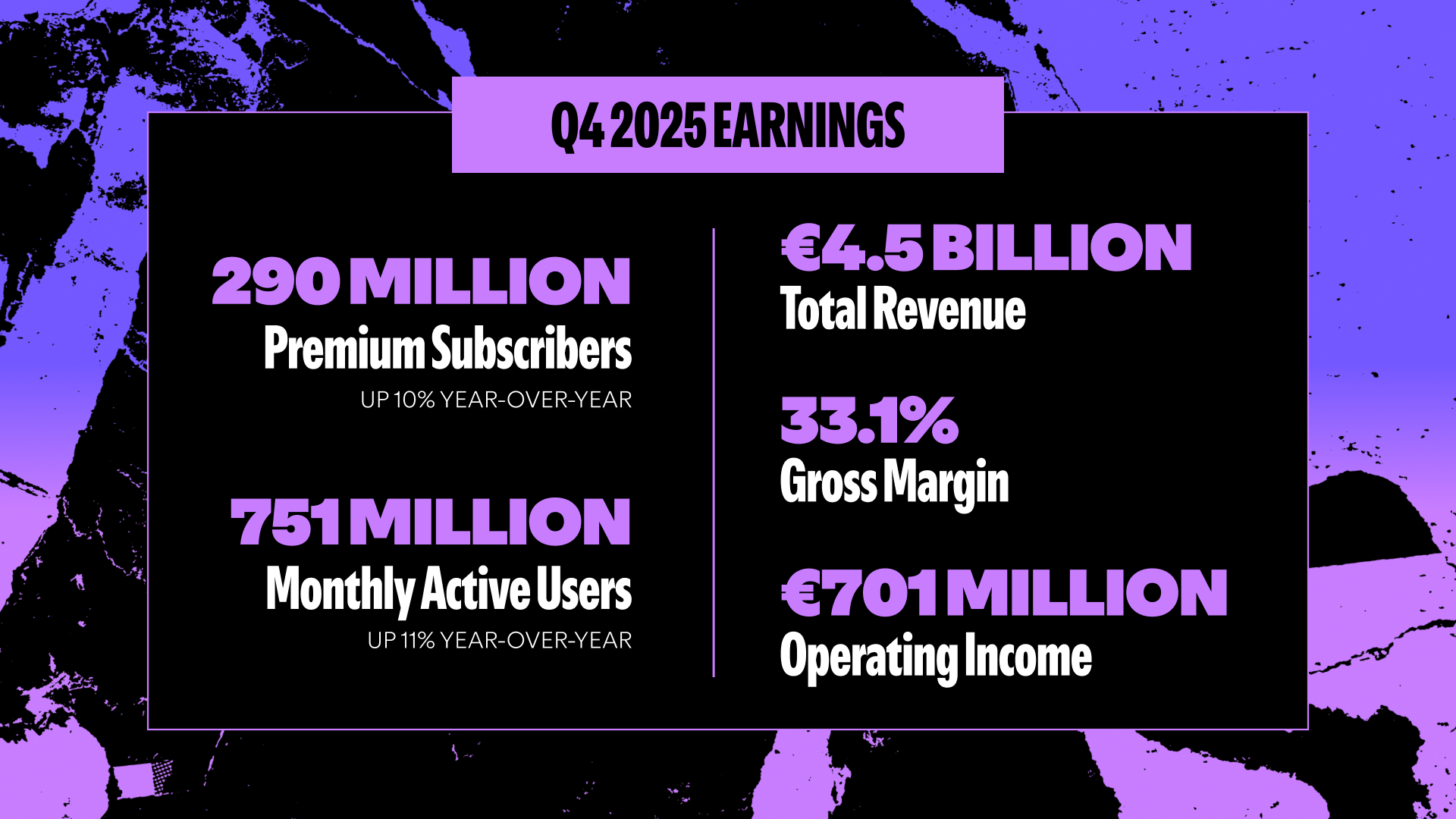

Apple has the hardware + OS. Amazon has Prime distribution. Google has Android + YouTube. Yet Spotify still describes itself as the world’s most popular audio streaming subscription service, and its scale keeps growing (e.g., Q4 2025: 290M Premium Subscribers, 751M MAUs).20

The takeaway isn’t “Spotify is magical.” It’s structural: even with massive distribution disadvantages, a focused specialist can win when it owns the user experience, personalization loop, and product identity.

Case 2: Amazon built its own meeting product (Chime) — then chose Zoom

This is one of my favorite “C” examples because it’s so brutal.

Amazon is not exactly short on engineers. It had its own meeting tool (Chime). And yet it moved to Zoom as the standard internal meeting app and started deprecating Chime for internal use. That’s the clearest possible signal: even the biggest incumbents don’t automatically win in every adjacent category.21

Why does this matter for our broader topic?

Because it shows that “the platform can ship it” is not the same as “the platform can replace it.”

Meetings are inherently cross-company. External guests matter. Reliability and simplicity matter. And neutrality matters.

Zoom itself leans into this by building interoperability with Microsoft Teams meetings (so enterprises don’t have to choose a single religion).22

That’s a classic startup survival move: embrace the ecosystem reality instead of fighting it.

Case 3: Google+ vs Facebook — the incumbent shipped, but the network stayed put

Sometimes the incumbent doesn’t just copy a feature — it tries to launch an entire competing product. And still loses.

Google+ is the clean case: Google tried to take on Facebook, and eventually shut Google+ down in February 2019.23

The lesson isn’t “Google is dumb.” The lesson is: in social/network categories, distribution is not the only moat — coordination is.

A social network is only valuable if the people you care about are already there. So even if Google+ offered a better UI or faster experience, the typical user faced a rational dilemma:

“Sure, I can move… but if my friends don’t move with me, I’ll end up alone in a digital ghost town.”

That’s the incumbency advantage in network markets: individuals prefer being where others are (network effects), and that creates a self-reinforcing loop. Each person waits for others to move first — and if everyone waits, nobody moves.

Imperial’s model uses a simple analogy: it’s like a crowd trying to cross a busy road. One person crossing alone feels risky. Crossing together is easier. But without a coordinated trigger, the crowd just keeps waiting on the same side. Even when a better option exists, the group gets stuck.

This also explains a counterintuitive point: when switching is always available (“I can join anytime”), people become more comfortable delaying the decision. They tell themselves: “I’ll check later.” And later never happens. Ironically, more frequent opportunities to switch can strengthen the incumbent’s grip, because it makes procrastination feel safe.

The big takeaway for our topic: there are categories where an incumbent can ship a respectable clone and still fail — not because the clone is bad, but because adoption requires coordinated migration. In network markets, the moat is the collective habit, not the feature list.24

What this means (and why it matters for AI): So yes: incumbents can move into your category. But “they shipped it” doesn’t automatically mean “you’re dead.”

If your product is:

loved for a specific workflow,

neutral across ecosystems,

embedded in how people coordinate with others,

and improving via real feedback loops,

…then the incumbent’s version can land with a thud, while you keep compounding.

That’s the “C” branch: the copy exists, but it doesn’t win.

8. (D) Regulation shifts the game → category re-opens | When the referee steps in ✅

This is the branch people underestimate — especially in Europe.

If the “kill mechanism” is distribution abuse (tying, self-preferencing, unfair access), regulation can reopen the market.

Google Shopping (self-preferencing as an abuse of dominance)

The European Commission’s Google Shopping decision is one of the clearest institutional documents describing self-preferencing dynamics.25

Amazon Marketplace commitments (seller data + Buy Box access)

The EU commitments show how regulators target data advantage and marketplace access — exactly Mechanism 5 and 2 in action.26

Slack vs Microsoft Teams bundling → commitments accepted

Slack publicly filed a complaint over tying Teams into Office.27

The European Commission later accepted commitments from Microsoft addressing Teams competition concerns (including suite versions without Teams, pricing differences, interoperability/portability measures).28

Why this matters for AI: if the assistant becomes the UI/OS layer, you will see more fights around tying, defaults, and access — and more regulatory attention.

9. (E) Coexistence → “good enough” + specialists win the edge | When bundling expands the market, not kills it ✅

Not every platform move ends in a kill shot.

A very common outcome is coexistence:

The incumbent ships a “good enough” baseline (often bundled).

And the specialist keeps winning the hard parts — the edge cases, the regulated workflows, the “if this breaks, someone gets fired” moments.

This is the outcome people underestimate because it doesn’t look dramatic. But economically, it’s massive: the baseline gets repriced, and the premium moves up-market.

Why coexistence happens (even when the platform is huge)

Different jobs, same category.

“Good enough” is fine for 80% of users. The remaining 20% have complex needs — compliance, collaboration across companies, audit trails, deep integrations, admin control, liability.Enterprises buy redundancy and risk reduction.

They don’t like single points of failure. They’ll happily run a bundled baseline and a best-of-breed tool in parallel.Incumbents optimize for the median. Specialists optimize for outcomes.

Platforms have to serve everyone. Specialists can serve one persona extremely well.

Case 1: Teams + Zoom — the suite wins internal defaults, specialists win “serious meetings”

Microsoft Teams is everywhere because it’s bundled and integrated into M365. But Zoom is still very much alive — and a big reason is that organizations end up using both.

Zoom literally documents “working across platforms” with Microsoft and provides interoperability so Zoom Rooms can join Teams meetings. That’s not “winner takes all.” That’s coexistence by design.29

Pattern: Teams becomes the default internal layer. Zoom keeps share where reliability, external guests, rooms, and meeting UX matter.

Case 2: Microsoft Word has “good enough” writing help — Grammarly still builds a big business

Microsoft has grammar checking and Editor inside its ecosystem. Yet Grammarly (now pushing into a broader “AI productivity platform” direction) still reports huge usage and real revenue.

Reuters reported Grammarly had 40+ million daily users and annual revenue exceeding $700M around its Superhuman acquisition story.30

And Grammarly’s own announcement repeats the same scale numbers (40M daily users, $700M+ revenue).31

Pattern: the platform covers the baseline for casual use; the specialist wins the “I do this all day, across apps, with higher stakes” layer.

Case 3: Microsoft Defender sets a baseline — specialists like CrowdStrike compete above it

Security is a perfect coexistence category because buyers hate risk and love layered defense.

Defender is deeply integrated into the Microsoft stack and becomes the default baseline in many environments. Meanwhile, specialists differentiate on cross-platform coverage, threat hunting, incident response, and operational workflows.

Even CrowdStrike positions a product explicitly to deploy alongside Microsoft Defender (“Falcon for Defender”). Whether you like the marketing or not, it’s a strong signal of how the market actually behaves: parallel stacks are normal.32

A more neutral lens: Microsoft Defender and CrowdStrike are both widely adopted, with different strengths and architectures (integration vs cloud-native specialization).33

Pattern: baseline bundled security + best-of-breed security for serious threat posture.

The AI twist is not that coexistence disappears — it’s that the baseline moves faster. Assistants will bundle more “generic intelligence” into the default experience: drafting, summarizing, simple analysis, basic automation. That will compress margins for anything that’s basically a clever UI on top of an LLM.

Coexistence remains likely where the product is not “intelligence,” but a workflow with responsibility: permissions, audit trails, system-of-record integration, reliability, and liability. In other words: the assistant can generate output, but a real business still needs a toolchain that can prove what happened, enforce policy, and survive edge cases.

What coexistence means for AI (and why it’s not “copium”)

As assistants become the front door, they’ll absorb the common workflows.

That will hurt every “feature-shaped” product. Prices compress. Differentiation evaporates.

But coexistence is the reminder that this is not automatically the end of startups. It’s a re-segmentation:

Baseline = bundled, cheap, ubiquitous

Premium = workflow depth, trust, compliance, auditability, integrations, domain edge cases

If you’re building where the premium lives, coexistence is not the consolation prize — it’s the plan.

Part III - Implications

10. The only predictor that matters

Here’s my strongest opinion in this whole piece:

The biggest risk is not “Big Tech copies you.”

The biggest risk is building something that can be copied as a feature.

If your product can be described as:

“X, but inside ChatGPT”

“Y, but built into Google Workspace”

“Z, but Microsoft bundles it”

…then you’re in the blast zone.

The “feature-shaped startup” checklist ⛔️

You’re at high A1 risk if most are true:

Your product is one step in a bigger workflow

You don’t own the system of record

You don’t own distribution (you’re dependent on one platform / one API)

Switching costs are low

Your differentiation is mostly “UX + prompt engineering”

Your data advantage is weak or non-exclusive

Your pricing is easy to undercut

In AI, the “prompt engineering” part is especially dangerous. Because as models improve, a lot of what looked like product differentiation becomes… a settings page.

The “workflow owner” checklist (how A2/E happens) ✅

You’re much more resilient if:

You own the workflow end-to-end (not just a step)

You own a system of record (or the permission layer around it)

You sit in compliance, procurement, trust, auditability

You have proprietary data rights / durable feedback loops

You integrate across ecosystems (not dependent on one)

You sell into a buyer with real risk (legal, security, finance, healthcare)

You become embedded into daily work (switching pain is real)

This is why “vertical B2B with insider founders” is not a cute thesis line. It’s a survival strategy.

Deep domain workflows have messy edge cases. Incumbents hate messy edge cases.

11. AI makes incumbents faster, but also creates new cracks

The interface layer shift is real — but it doesn’t mean startups are dead. AI makes the platform move downstream faster. True.

But it also creates new cracks that startups can exploit:

1) General models are broad. Workflows are narrow.

Models are good at language. Companies pay for outcomes.

“Draft this legal clause” is broad.

“Draft this legal clause that passes our internal policy, maps to our jurisdiction, logs the audit trail, and won’t get the GC fired” is narrow.

2) Trust and liability don’t scale like code

In regulated B2B, the product is not “smartness”. The product is risk containment.

That creates room for specialists.

3) Distribution is changing — not just consolidating

Yes, assistants create a new choke point. But they also create a new distribution channel for startups (if you’re positioned correctly).

The trick is: don’t be a toy inside someone else’s store. Be the thing that owns the workflow and uses the assistant as an interface.

12. So what do you tell an investor (without selling)?

If an Angel asks: “Aren’t you afraid OpenAI/Google will just copy your startups?”

A professional answer is not a slogan. It’s a framework:

Acknowledge the risk (don’t minimize it)

Explain the mechanisms (bundling, self-preference, policy, pricing, data)

Show the outcomes (A1/A2/B/C/D/E)

Explain what you underwrite (you avoid feature-shaped startups; you want workflow owners)

Explain how you position (multi-platform, deep vertical, data rights, compliance, distribution strategy)

The strongest stance is:

“We assume incumbents will move downstream. That’s the baseline.

Our job is to invest where ‘downstream’ doesn’t automatically equal ‘dead’.”

13. Practical advice for founders (what I would do)

If you’re building in AI and you want to be alive in 36 months:

1) Don’t build a feature. Build a workflow.

If you can’t explain why you still exist after “Microsoft ships it in Copilot,” you don’t have a company yet.

2) Own a painful edge case

Pick the part incumbents hate: compliance, audit, procurement, messy integrations, change management, deeply specific domain constraints.

3) Own the data rights, not just the data

It’s not “we have data.” It’s “we have permissioned, defensible access to data that improves the product over time.”

4) Reduce single-platform dependency

If you are fully dependent on one model provider, one marketplace, one API… you are a policy change away from a crisis.

5) Treat incumbents as a distribution channel, not a competitor

Integrate, partner, sell through, ride their wave — but don’t let them own your identity.

14. The real conclusion (and the honest one)

Yes: incumbents can kill startups.

But the deeper truth is:

Incumbents mainly kill feature-shaped startups.

Workflow-shaped startups are harder to kill, and often end up in A2, E, or B.

AI makes the playbook faster — but it doesn’t change the playbook.

So if you’re a founder: the question is not “Will they copy us?”

The question is: “Can they copy us as a feature?”

If the answer is yes, fix that now — while you’re still small.

🎚️🎚️🎚️🎚️ Producer’s Note - “Rolling Stone”

The original, the cover, and the loop

1950: Muddy Waters records a blues single called “Rollin’ Stone” on Chess.

That title itself sits on an older cultural phrase (“rolling stone…”) that’s been around forever — blues guys didn’t invent it either, they remixed it.34

1962: A young London blues band needs a name. According to the common origin story, Brian Jones is on the phone with Jazz News, spots a Muddy Waters record on the floor, sees the track “Rollin’ Stone,” and blurts out the band name. 35

(At first they even used “The Rollin’ Stones” — before the “g” showed up.)36

1965: Bob Dylan releases “Like a Rolling Stone”. 37

Important detail: this does not inspire the Stones’ name — they existed already. But it shows how the same phrase travels across decades and genres.

1995: The circle closes in the most satisfying way: the Rolling Stones cover Dylan’s “Like a Rolling Stone” and release it on Stripped. 38

(Recorded during their 1995 small-venue shows; releases/editions vary, but the point stands: the band named after a Muddy Waters track ends up covering the Dylan song with the same phrase in the title.)

Keep rolling.

Fab 🏍️

LinkedIn | Insta | Twitter | Studio⍺

Appendix — The “outcome tree” in one view (with examples)

A1: Copied/bundled → dies

OS/suite tying and default distribution examples (U.S. v. Microsoft era).

Source: https://www.justice.gov/atr/us-v-microsoft-courts-findings-fact (Department of Justice)“Sherlocking” type dynamics.

Source: https://techcrunch.com/2025/06/10/wwdc-2025-everything-that-apple-sherlocked-this-time/ (TechCrunch)

A2: Copied → pivots/wins

Dropbox competing with platform providers (explicit in filings).

Source: https://investors.dropbox.com/static-files/eaffdb7c-727a-40c6-9308-1c1c062d2b30 (Dropbox)Foursquare pivot to location intelligence.

Source: https://d3.harvard.edu/platform-digit/submission/foursquare-using-crowdsourcing-to-fuel-a-turnaround/ (Digital Data Design Institute at Harvard)Snapchat vs Instagram Stories copy dynamic.

Source: https://www.theverge.com/2016/8/2/12348354/instagram-stories-announced-snapchat-kevin-systrom-interview (The Verge)

B: Bought

DeepMind, Waze, Instagram, Siri.

Source: https://www.reuters.com/article/business/google-to-buy-artificial-intelligence-company-deepmind-idUSBREA0Q032/ (Reuters)

Source: https://www.theguardian.com/technology/2013/jun/11/google-buys-waze-maps-billion (The Guardian)

Source: https://www.reuters.com/article/technology/facebook-to-buy-instagram-for-1-billion-idUSBRE8380M9/ (Reuters)

Source: https://techcrunch.com/2010/04/28/apple-buys-virtual-personal-assistant-startup-siri/ (TechCrunch)

D: Regulation changes the game

Google Shopping decision; Amazon commitments; Teams commitments.

Source: https://ec.europa.eu/competition/antitrust/cases/dec_docs/39740/39740_14996_3.pdf (European Commission)

Source: https://ec.europa.eu/commission/presscorner/detail/en/ip_22_7777 (European Commission)

Source: https://ec.europa.eu/commission/presscorner/detail/en/ip_25_2048 (European Commission)

Sources

https://studioalpha.substack.com/publish/post/189341858?back=%2Fpublish%2Fposts%2Fdrafts

Source: https://www.wsj.com/tech/ai/anthropic-dials-back-ai-safety-commitments-38257540 (Wall Street Journal)

Source: https://openai.com/index/introducing-the-gpt-store/ (OpenAI)

Source: https://blog.google/products-and-platforms/products/workspace/google-gemini-workspace/ (blog.google)

Source: https://claude.com/blog/artifacts (Claude)

Source: https://www.theverge.com/news/693342/anthropic-claude-ai-apps-artifact (The Verge)

AI assistant

Interface-first.

You talk to it. It answers, drafts, summarizes, explains. It can optionally use tools, but the core thing is: conversation + output.

Examples: ChatGPT, Claude, Gemini (as chat products), Copilot chat mode.

AI agent

Action-first.

It doesn’t just respond — it plans + executes steps toward a goal, often using tools (browser, calendar, APIs, code, CRM), sometimes running for minutes and checking results.

Examples: “Book me a flight and file the expenses,” “Monitor competitors weekly and alert me,” “Find leads, enrich them, draft outreach, push into HubSpot.”

The clean mental model

Assistant = brain + chat UI (help me think / write / decide)

Agent = brain + autonomy + tools (help me do things)

https://www.ft.com/content/d077e9c6-1573-46dc-8658-3db3aaf7cdfb

Source:

https://newsroom.spotify.com/2026-02-10/spotify-q4-2025-earnings/(Spotify Newsroom)Source:

https://s29.q4cdn.com/175625835/files/doc_financials/2025/q4/Spotify-20-F-Filing.pdf(Spotify 20-F)Source:

https://www.reuters.com/technology/spotifys-daniel-ek-become-executive-chairman-soderstrom-norstrom-named-co-ceos-2025-09-30/(Reuters)

Source:

https://www.businessinsider.com/amazon-zoom-main-meeting-app-microsoft-365-2025-2(Business Insider)

Source:

https://library.zoom.com/admin-corner/third-party-integrations/zoom-and-microsoft-working-across-platforms(Zoom)

https://www.theguardian.com/technology/2019/feb/01/closure-google-plus-everything-you-need-to-know

https://www.imperial.ac.uk/business-school/ib-knowledge/strategy-leadership/why-did-google-fail/

Source: https://library.zoom.com/admin-corner/third-party-integrations/zoom-and-microsoft-working-across-platforms (Zoom)

Source: https://support.zoom.com/hc/en/article?id=zm_kb&sysparm_article=KB0067180 (Zoom Support)

Source: https://www.reuters.com/business/grammarly-acquires-email-startup-superhuman-ai-platform-push-2025-07-01/ (Reuters)

Source: https://www.grammarly.com/blog/company/grammarly-announces-growth-financing/ (Grammarly)

Source: https://www.crowdstrike.com/en-us/platform/endpoint-security/falcon-for-defender/ (CrowdStrike)

https://www.wiz.io/academy/cloud-security/microsoft-defender-vs-crowdstrike-falcon

Source: https://en.wikipedia.org/wiki/Rollin%27_Stone_(Muddy_Waters_song) (Wikipedia)

Source: https://en.wikipedia.org/wiki/The_Rolling_Stones (Wikipedia)

Source: https://en.wikipedia.org/wiki/The_Rolling_Stones (Wikipedia)

Source: https://en.wikipedia.org/wiki/Like_a_Rolling_Stone (Wikipedia)

Source: https://en.wikipedia.org/wiki/Stripped_(Rolling_Stones_album) (Wikipedia)