"China Is Killing Europe"

Is Macron right — or is China only exposing what Europe has spent twenty years avoiding?

Emmanuel Macron recently said China is “literally killing a large part of the European industry.” It is a sentence built to travel: clear villain, clear victim, no need to inspect the crime scene too closely. 1

He may even be partly right. China is subsidising, overbuilding, exporting, and putting real pressure on European industry.

But blaming the other side usually says something about the person doing the blaming. We learned this quite early in school. Apparently it remains useful in geopolitics.

So the question is not only whether Macron is right. The question is why Europe now sounds like the victim in a story it helped write.

1. Europe enters this fight tired

Europe is starting to talk tougher about China. Fine. But Europe is not entering this fight from a position of strength. It is entering it with weak growth, expensive energy, an unresolved war on the continent, higher defence costs, and a political class that has spent years confusing regulation with strategy.

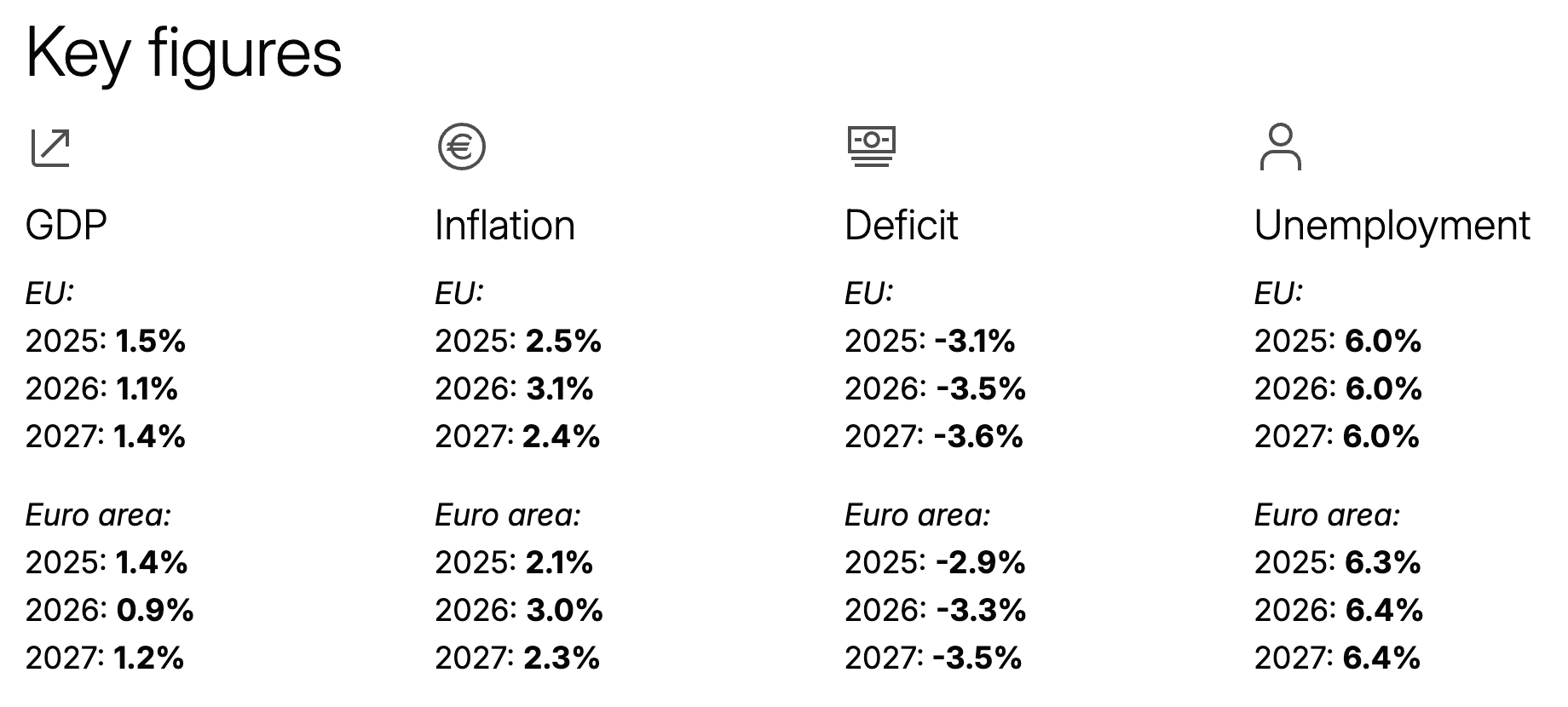

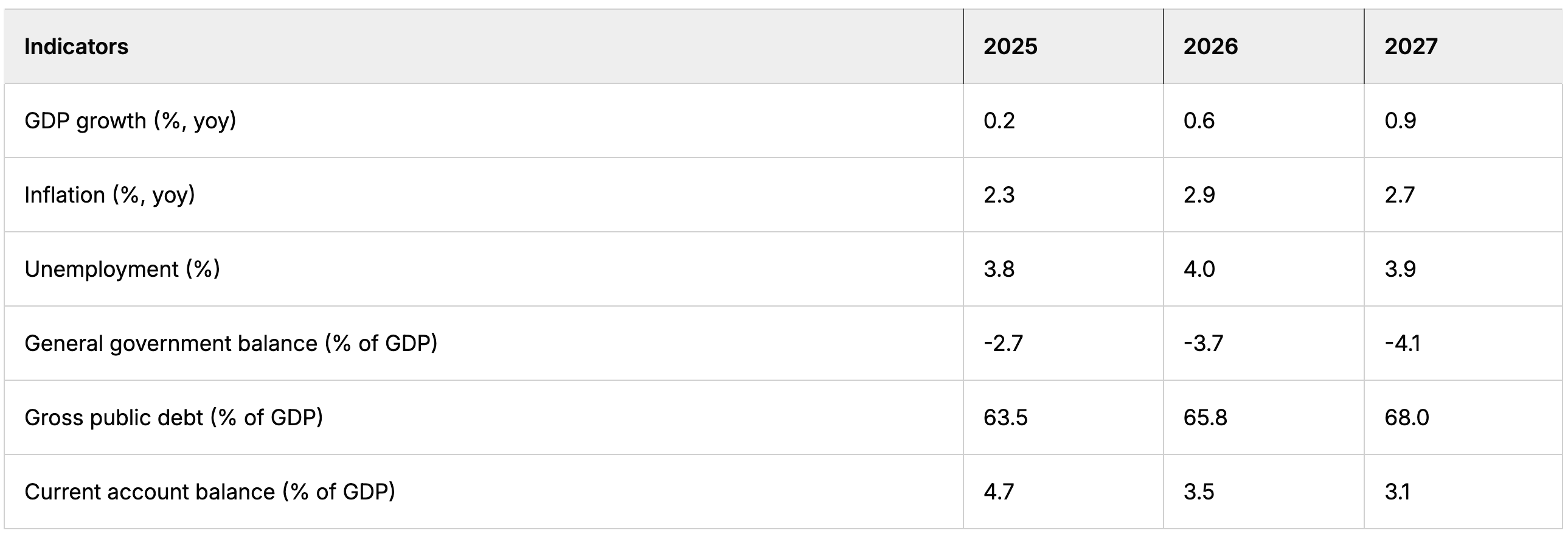

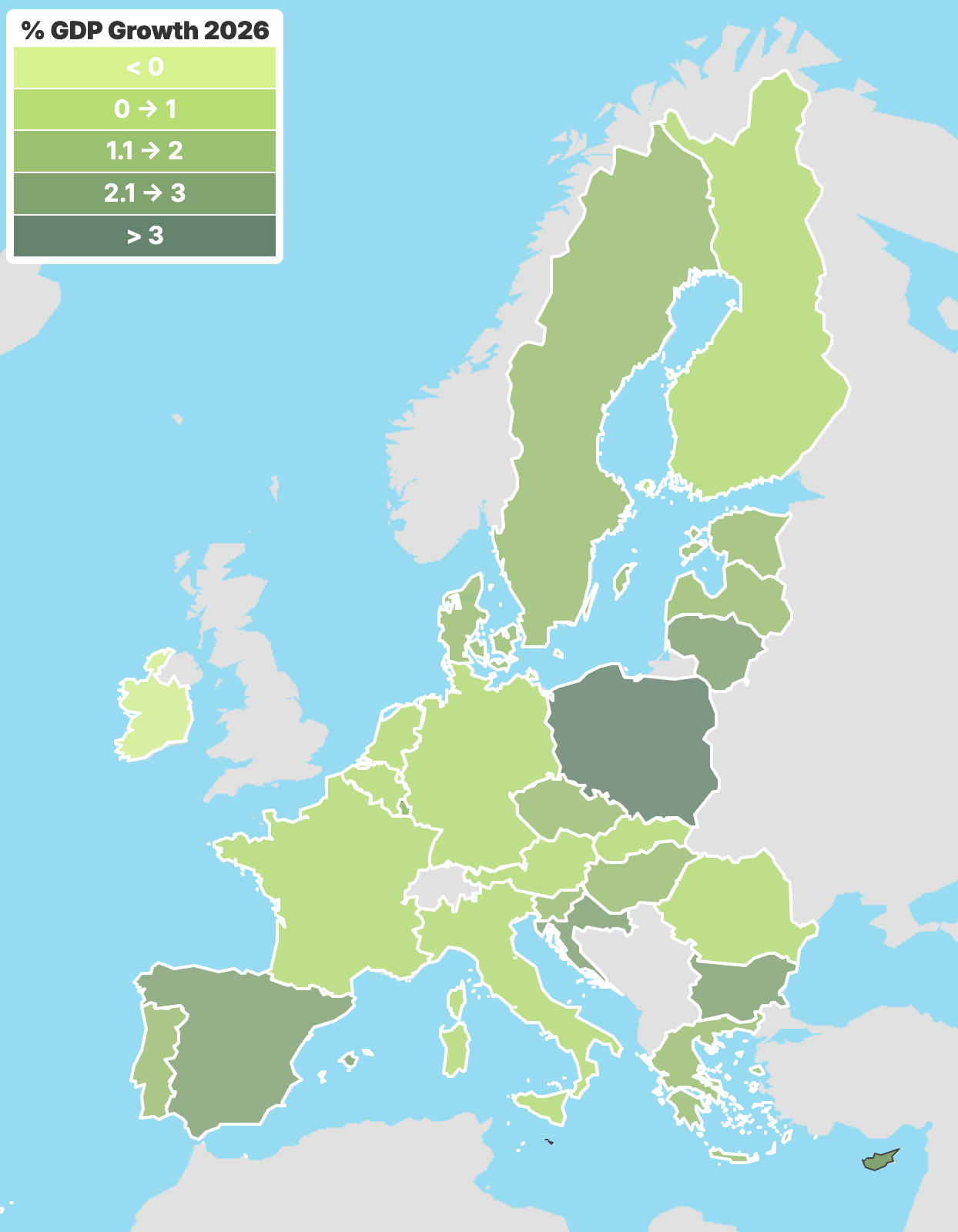

The European Commission expects EU GDP growth to slow to 1.1% in 2026. Germany, after two years of recession and weak growth of 0.2% in 2025, is expected to grow only 0.6% in 2026. That is not a recovery. That is a patient sitting up in bed and being congratulated for movement.23

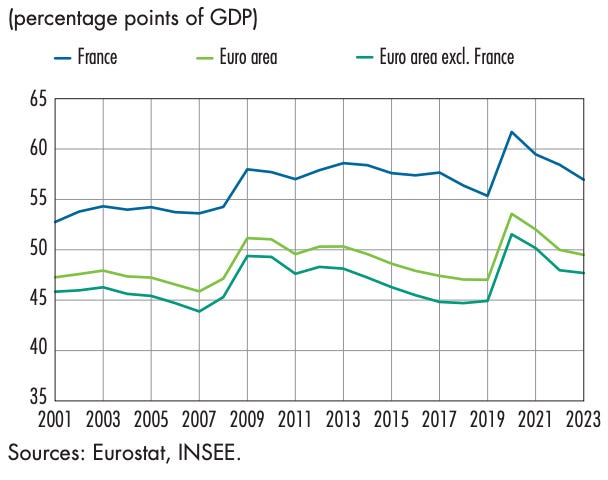

France has another problem: the size of the state. In 2024, public spending in France stood at 57.2% of GDP. Germany’s general government expenditure reached 49.5% of GDP. These are not small numbers. When the state absorbs around half the economy, and the result is still weak schools, slow trains, broken infrastructure, and endless administrative friction, the issue is no longer “we need more public money”. The issue is output.4

Savoir vivre: Changes in public spending in France, the euro area, and the euro area excluding France

Germany is a good example because the gap between reputation and reality has become hard to ignore. Deutsche Bahn’s long-distance punctuality was 63.4% in H1 2025. The federal audit office said only 69 of 280 planned bridge refurbishments were completed in 2024. KfW’s 2025 Municipal Panel put Germany’s municipal investment backlog at €215.7bn, with schools alone accounting for €67.8bn. This is what makes the China debate uncomfortable. China is not hitting a healthy European system. China is hitting a slow, expensive one.56

Jamie Dimon put the broader decline more brutally. Speaking in Dublin, he said Europe had fallen from 90% of US GDP to 65% over 10 or 15 years. The exact comparison can be debated. The direction is harder to dismiss. IMF work points in the same direction: Europe’s GDP per capita is around 72% of the US level, and much of the gap comes from lower productivity and a fragmented internal market. That is the background before China even enters the picture.78

Plainly said: It looks like things have been going downhill since the Euro monetary union.

2. China is now visible in Europe’s industrial mirror

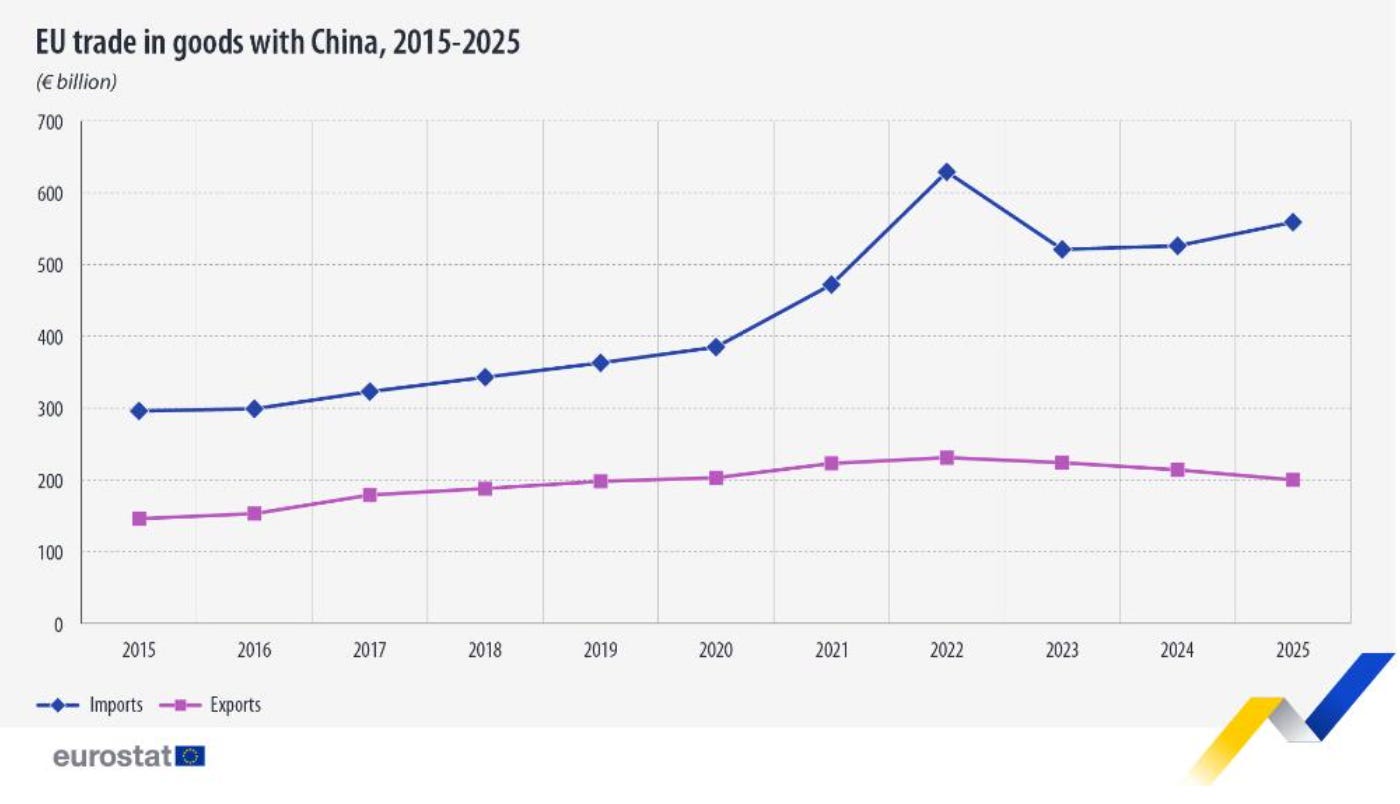

The simple concern: Europe is becoming more worried about its dependence on China. That concern is justified. The EU’s goods trade deficit with China reached €359.8bn in 2025. In Q1 2026 alone, the deficit reached €98bn, the highest quarterly level since Q3 2022. It is a scorecard.910

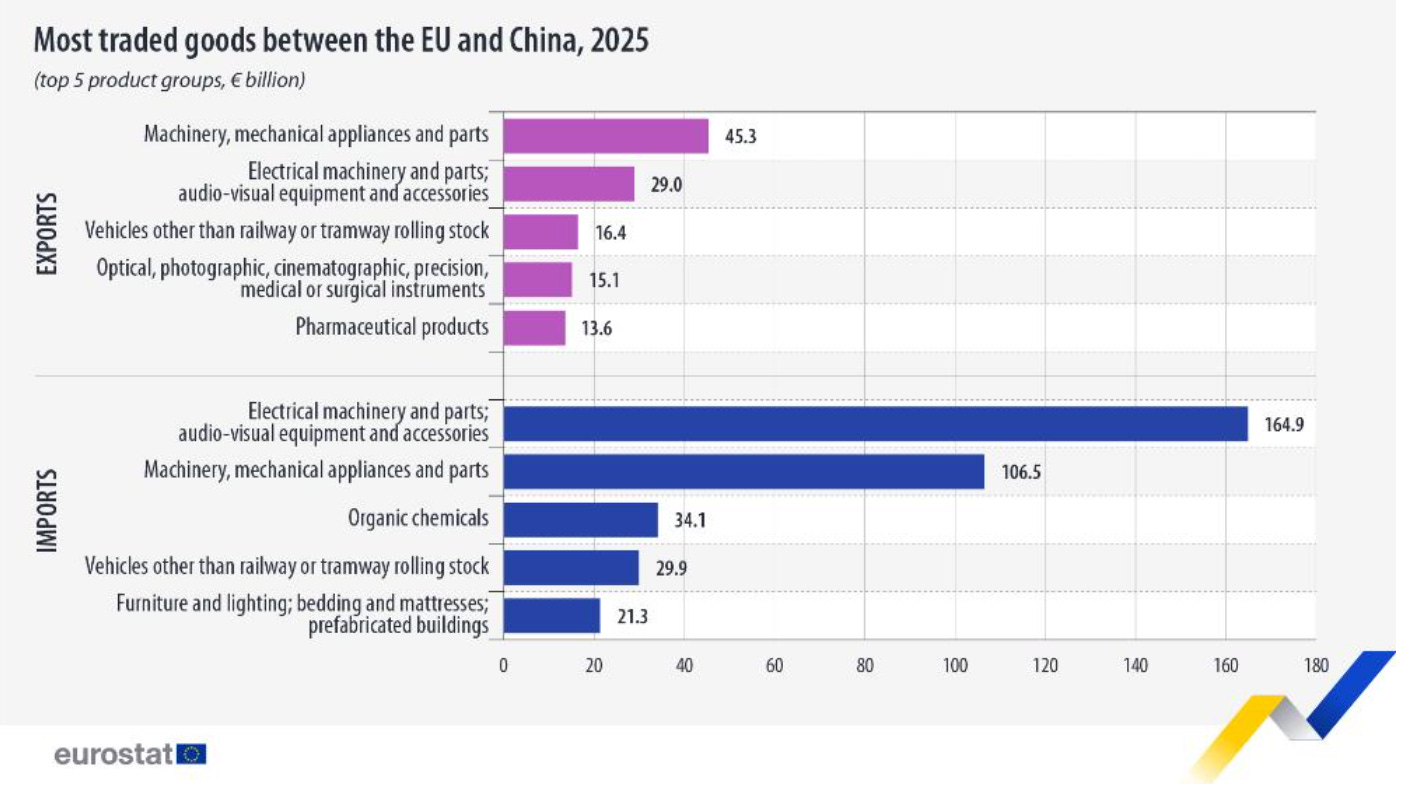

For decades, Germany and parts of Europe were the global reference point for cars, machinery, chemicals, specialised components, and industrial systems. Now China is moving into many of the same categories. China is becoming “Germany in the global supply chain” and replacing Europe in areas where German and European manufacturing used to be strong. Yes, that hurts.

The public fight is focused on electric vehicles because cars are visible. German brands are not just companies; they are national furniture. EVs also sit at the intersection of climate policy, jobs, software, batteries, industrial policy, and pride. When Chinese EVs enter Europe at scale, the reaction is therefore not only economic but psychological.

The EU has imposed definitive countervailing duties on battery electric vehicles imported from China, after concluding that China’s BEV (Battery Electric Vehicle) value chain benefits from unfair subsidies and threatens economic injury to EU producers. That may be justified. But cars are only the cleanest version of the problem. China has built a manufacturing system Europe struggles to match: scale, subsidies, supplier depth, domestic competition, export discipline, and increasingly strong engineering. Europe has committees. The gap is visible.11

3. Tariffs can buy time. They do not create competitiveness.

Europe now wants stronger trade defence tools. That is understandable. No serious economy can ignore subsidised competition forever. Letting strategic industries disappear and then discovering dependence during a crisis is negligence. But a tariff only buys time. It does not fix high energy costs. It does not fix weak productivity. It does not fix fragmented capital markets. It does not make European software companies scale faster. It does not make permitting move at Chinese speed. And it does not turn a protected incumbent into a serious competitor.

James Kynge makes the sharper point in his podcast. His fear is that Europe puts up trade barriers against China and ends up protecting the very problems that created the weakness:

huge inefficiencies,

high energy costs,

high labour costs,

restrictive labour laws,

restrictive investment laws,

and very low productivity.12

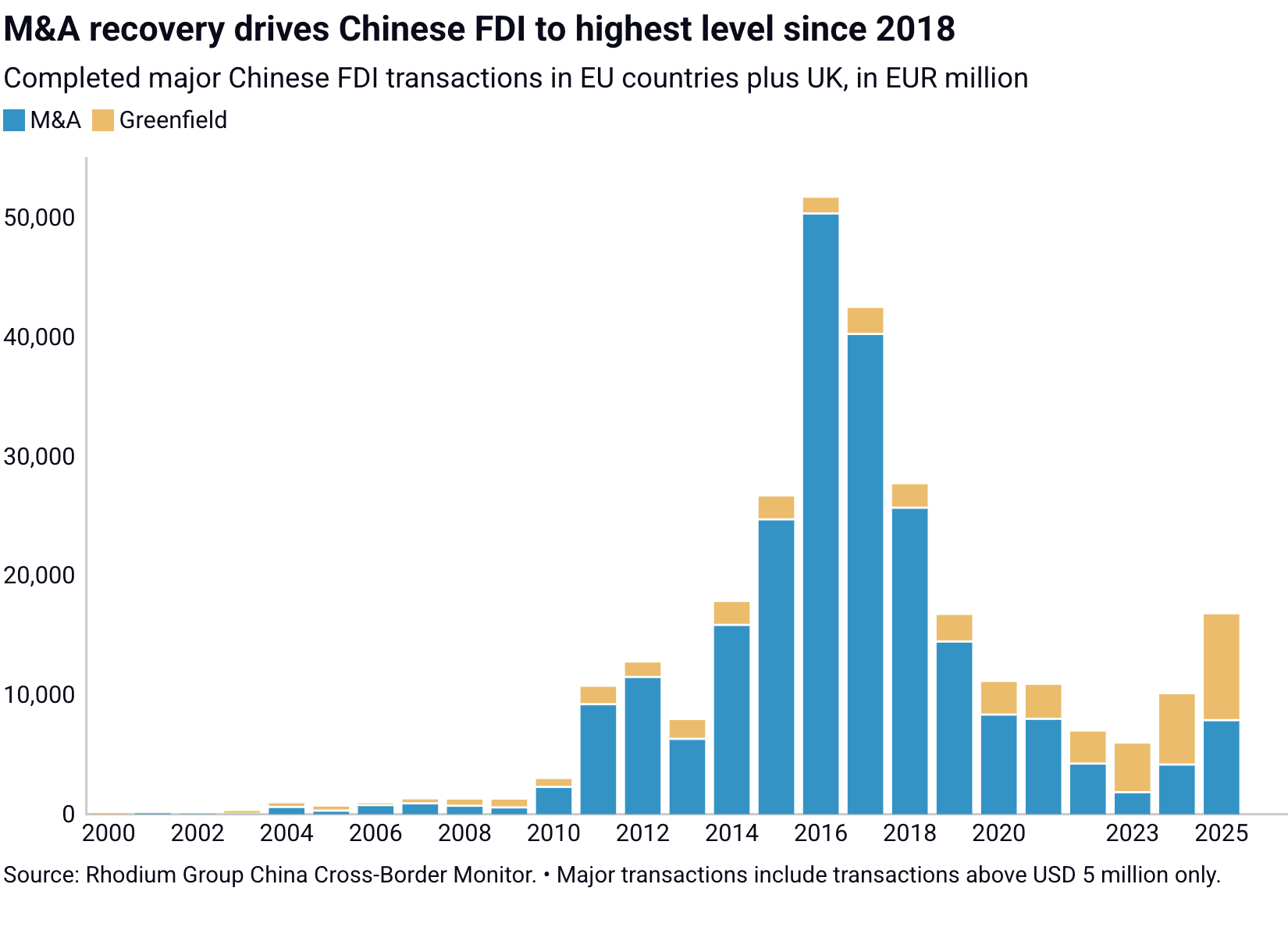

If Europe blocks Chinese imports, Chinese companies can still move production into Europe. That is already happening. Rhodium Group and MERICS report that Chinese direct investment in Europe rose to €16.8bn in 2025, the highest level since 2018. The automotive sector alone attracted €7.6bn, with 93% focused on the EV supply chain.13

So the tariff question becomes more awkward. If Chinese EVs are imported from China, Europe can tax them. If Chinese EVs are produced in Hungary, Spain, France, or Germany, the story changes. Europe may get factories, jobs, and ribbon-cutting photos. It may not get European champions. It may simply get Chinese industrial capability operating inside Europe’s borders.14

4. Germany is trapped inside the argument

Germany sits in the middle of this problem. It wants Europe to defend industry. It also wants to avoid a trade conflict that damages German companies in China. The transcript captures this directly: many of Germany’s biggest companies still have deep exposure to China, and that makes Berlin cautious.

That is the German trap. Germany helped build Europe’s China exposure. For years, China was a market, supplier, manufacturing base, and profit machine. Now China is also a competitor. That changes the relationship. The same country that bought German cars is now producing electric vehicles that make parts of the German model look old.15

The old German model was built around engineering depth, export discipline, industrial employment, affordable energy, and access to global markets. Several pillars are now under pressure at once. Energy is more expensive. China is more competitive. US industrial policy is more aggressive. Software matters more in cars and industrial systems. AI changes productivity expectations. And Europe’s internal market remains less integrated than it looks from a Brussels slide deck.

This is why Europe’s China policy risks becoming confused. France wants more protection. Germany fears retaliation. Southern Europe wants jobs and investment. Eastern Europe may welcome Chinese factories. Brussels wants strategic autonomy. Everyone agrees Europe needs to become stronger. Nobody wants to pay the transition cost. The minutes will be excellent.16

Pretty tricky.

5. China can hit back

A trade war with China is might be not good idea. China has tools such as brandy, pork, agriculture, critical minerals, and rare earths. That is the right list.

China has already targeted EU brandy in the wake of the EV tariff fight. Reuters reported that China imposed temporary anti-dumping measures on EU brandy in October 2024, hitting French brands including Hennessy and Rémy Martin. In 2025, China also placed initial anti-dumping duties on EU pork imports, deepening the trade tensions that followed the EV dispute.1718

Agriculture matters because Europe’s political economy is not a clean spreadsheet. A French cognac producer, a Spanish pork exporter, a German carmaker, a Hungarian battery plant, and a Dutch port operator do not experience China policy in the same way. China knows that. It can apply pressure sector by sector. Europe then gets what it does best: domestic fights about who should suffer first.

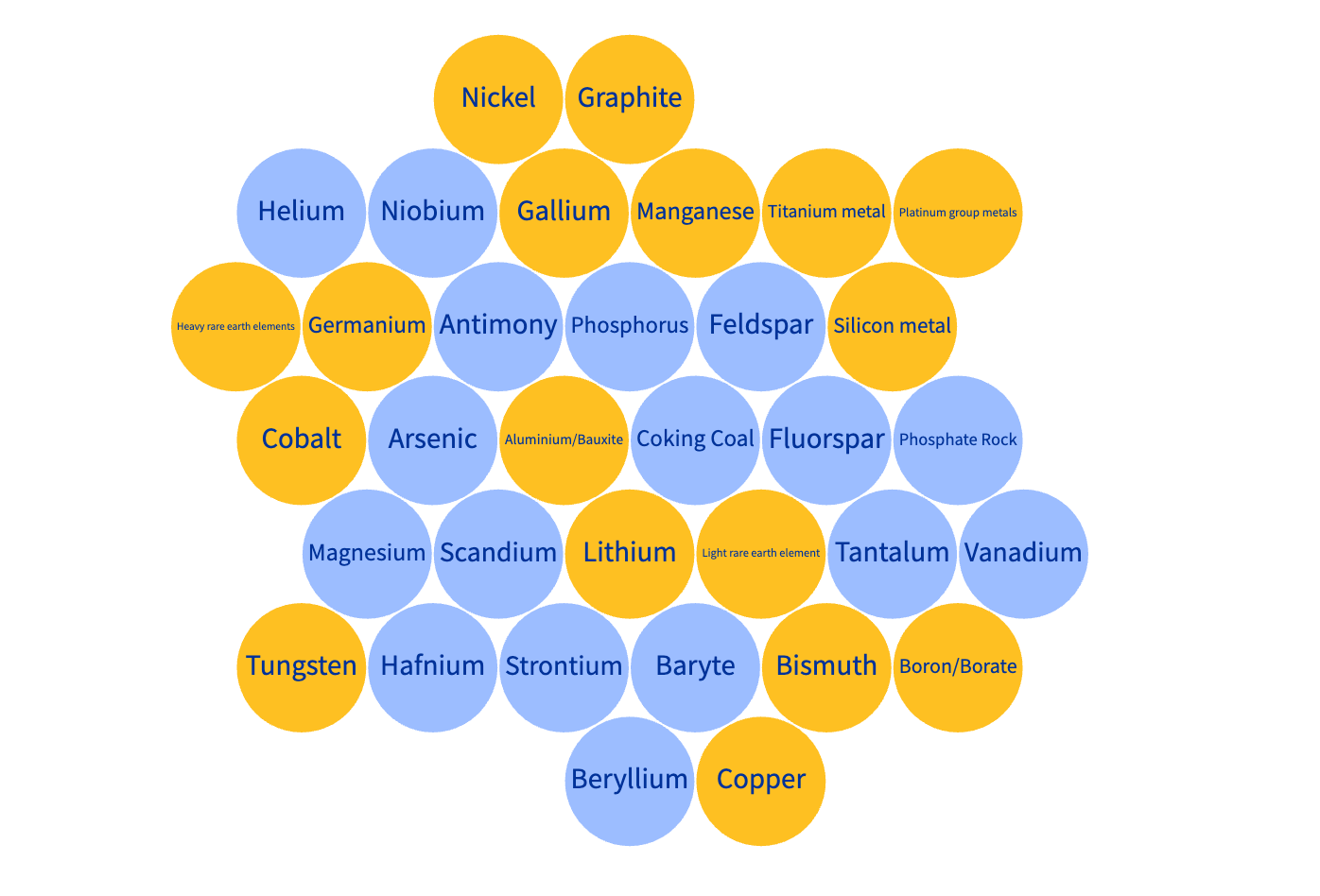

The more serious exposure is critical raw materials. The Council of the European Union says China provides 100% of the EU’s supply of heavy rare earth elements. These materials matter for defence, EVs, wind turbines, electronics, motors, sensors, and industrial systems. That is not a dependency. That is a leash.19

Strategic critical raw materials

(orange)

So before Europe talks itself into a trade war, it should ask one simple question: what happens on day three after China responds? If the answer is another summit, the strategy is not ready.

Really tricky.

6. The AI layer makes this worse

The old industrial fight was about cars, machinery, chemicals, energy, labour cost, and supply chains. The next industrial fight adds AI. This is where Europe’s position looks worst.

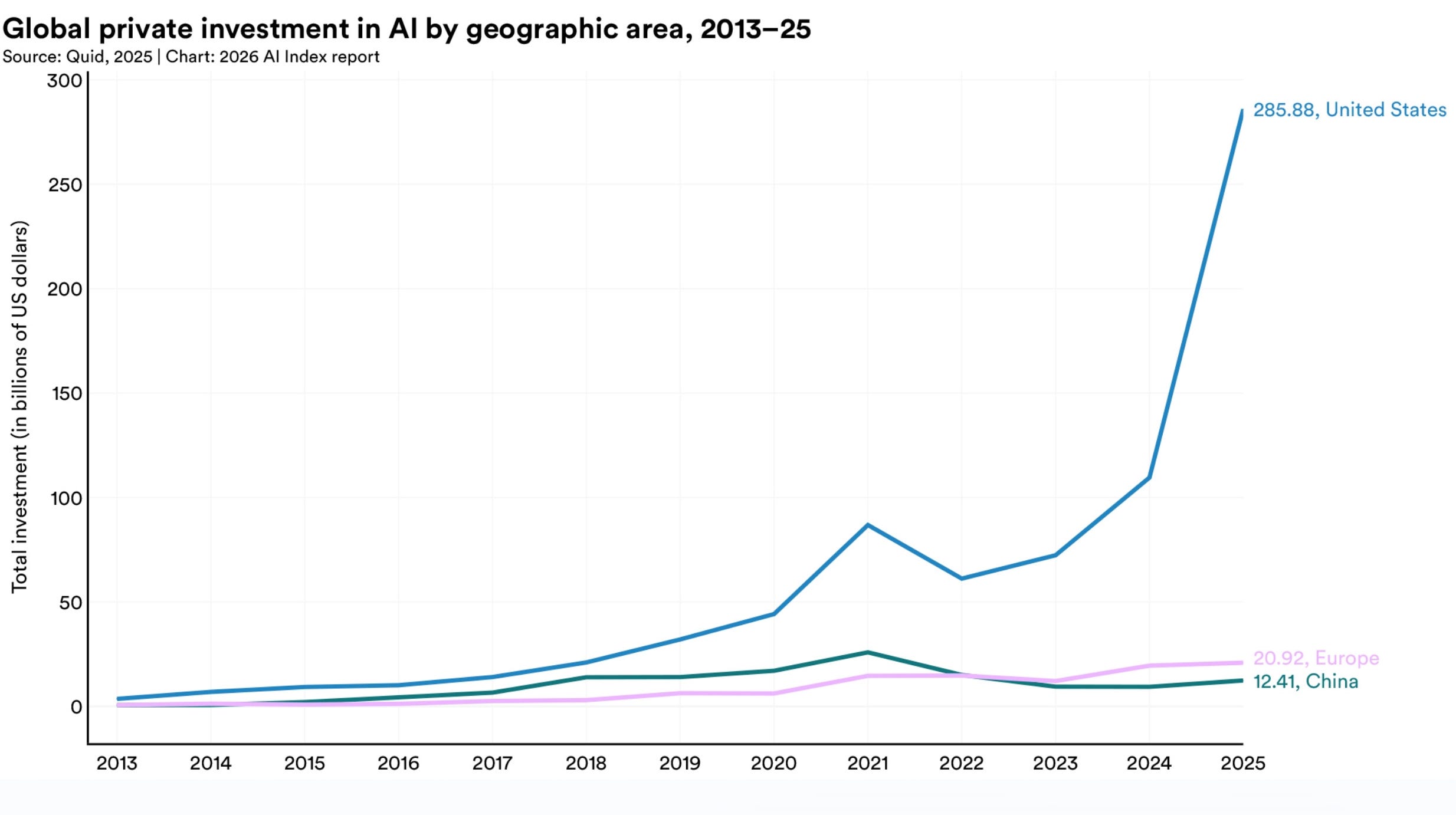

According to the Stanford 2026 AI Index, US private AI investment reached $285.9bn in 2025. The US invested 23 times more private capital into AI than China. Stanford also notes that US generative AI investment exceeded the combined total of China and Europe by a wide margin.20

This is the capital map. The US has the hyperscalers, frontier labs, chip access, enterprise software giants, and the largest venture market (91% in Q1/2026 as written in our Quarterly Investor Letter). China has state coordination, manufacturing scale, engineering depth, domestic deployment, and the ability to connect AI with industrial production. Europe has talent, universities, research, and speeches about sovereignty. Talent matters. Speeches less so.

AI is not an isolated tech sector. It becomes part of industrial competitiveness. It changes how cars are designed, how factories are run, how logistics are managed, how software is built, and how companies learn. The next industrial base is software, data, compute, energy, capital, distribution, and speed. Europe is weak on too many of those at once.

Large AI infrastructure announcements are therefore useful but not sufficient. France attracting major AI investment pledges is positive. Europe needs compute, data centres, energy capacity, and sovereign options. But compute does not automatically create category-leading companies. A data centre is infrastructure. It becomes strategically useful only when it supports products, customers, talent density, venture capital, procurement, and fast adoption. Otherwise it is concrete with a press release.21

7. The question Europe should ask

Europe should not be passive about China. China uses state support, industrial strategy, export scale, critical-material leverage, and domestic market power. Europe has every right to defend itself against unfair competition.

But blaming China is the easy version. China did not create Europe’s productivity gap. China did not fragment Europe’s capital markets. China did not make France’s public spending reach 57% of GDP. China did not make Germany slow in software-defined cars. China did not stop Europe from building deeper AI capital markets. China did not stop Europe from implementing the Draghi report. China is exposing the weaknesses Europe built for itself.22

That is the better frame. Trade defence should buy time for reform. It should not become a blanket over weak execution. A serious European response would defend genuinely strategic industries, fix the internal barriers that stop companies from scaling across one real market, and treat AI, software, compute, energy, and industrial policy as one connected competitiveness problem.23

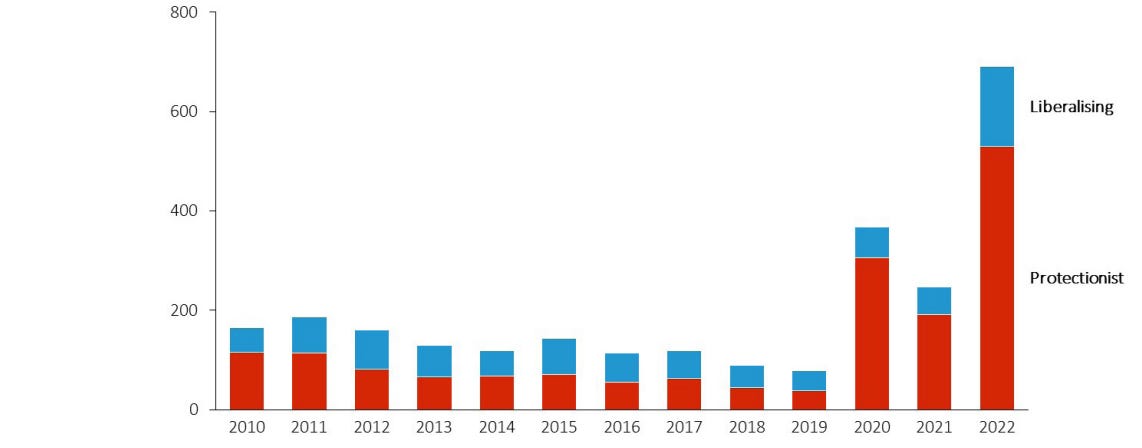

Trade policy interventions in Europe

Without that, tariffs become theatre. The uncomfortable lesson for founders is simple: do not wait for Europe to protect you, finance you, or move fast enough around you. Build for the real world: international capital, fast product cycles, hard technical differentiation, distribution outside your home market, and customers who pay because the product works. That is the part Europe still controls.

Europe is not enough as a default market. That is why we help founders build for the US from day zero. Apply here.

🎚️🎚️🎚️🎚️ Producer’s Note

Europe and China, basically:

Je t’aime… moi non plus. (“I love you… me neither.”)

Love, dependence, suspicion, trade deficits, and just enough drama to keep Brussels busy.

Freedom would be nice.

Best,

Fab 🗽

LinkedIn | Insta | X

StudioAlpha Capital is a Delaware-structured pre-seed venture fund backing AI-native B2B software startups at day zero. Legal counsel: Cooley LLP. Fund administration: AngelList.

Sources

Source: https://www.ft.com/content/cccbe89e-449d-4428-8704-be98351b716c?syn-25a6b1a6=1

Source: https://www.reuters.com/world/cross-border-challenges-widen-wealth-gap-between-europe-us-imf-study-finds-2024-11-14/

Source:

Source: https://www.reuters.com/markets/commodities/china-puts-anti-dumping-measures-brandy-imports-eu-2024-10-08/