⛈️ The Perfect Storm PART I

⛈️ The Perfect Storm PART I

How the 2008 Financial Crisis Is Still Affecting Us Today

Welcome to Roll-Right-In/Money, brought to you by Tim, Max, and Fabian from Oceanic.us Partners and StudioAlpha.capital. We're here to keep you informed on the latest financial market updates and their implications for founders and investors. In this week's blog, we explore the tense macroeconomic situation impacting companies, startups, investors, and soon, consumers.

This blog is a 7-min read.

The current crisis looks like the perfect storm with:

High inflation

High interest rates

Banking sector tremendously under pressure

States applying emergency law

SEC tackling Crypto Space

OPEC+ announced production cuts

Recession around the corner

Why it matters: This is what happens when you print too much money, have a pandemic, lower interest rates to zero, then raise rates incredibly fast to combat the inevitable inflation. These factors and more have contributed to a massive reset globally in valuations, with the unprofitable private tech companies and small banks taking the brunt of it. Perhaps not the worst thing, as we will explain.

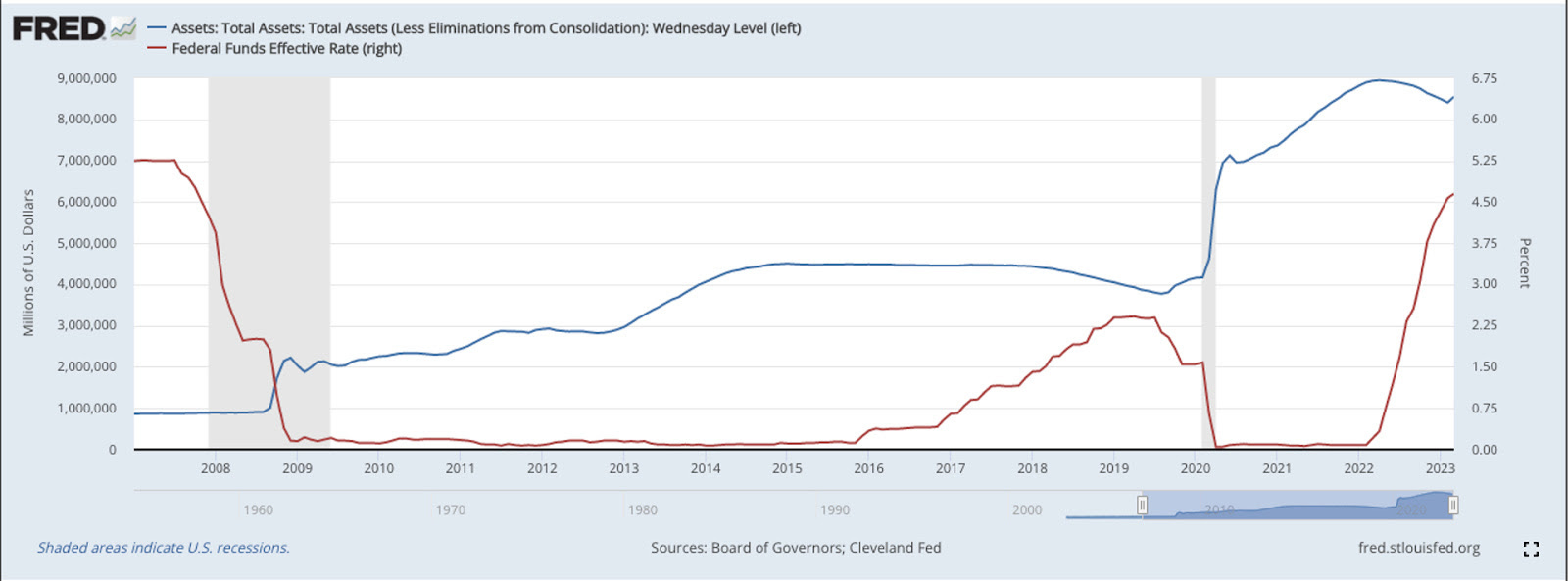

Let’s look back: In recent years, we've witnessed the culmination of long-term trends, such as the debt cycle and interest rate downtrend, which began in the early 1980s. The 2008 financial

crisis laid the foundation for the current situation, with the Federal Reserve implementing aggressive measures to stabilize markets and maintain artificially low rates. Despite tapering efforts, the COVID-19 pandemic led to further balance sheet expansion and unprecedented policy measures, surpassing all previous actions.

Pic 1: the brief history of interest rates and monetary policy since the financial crisis (Data: fred.stlouisfed.org)

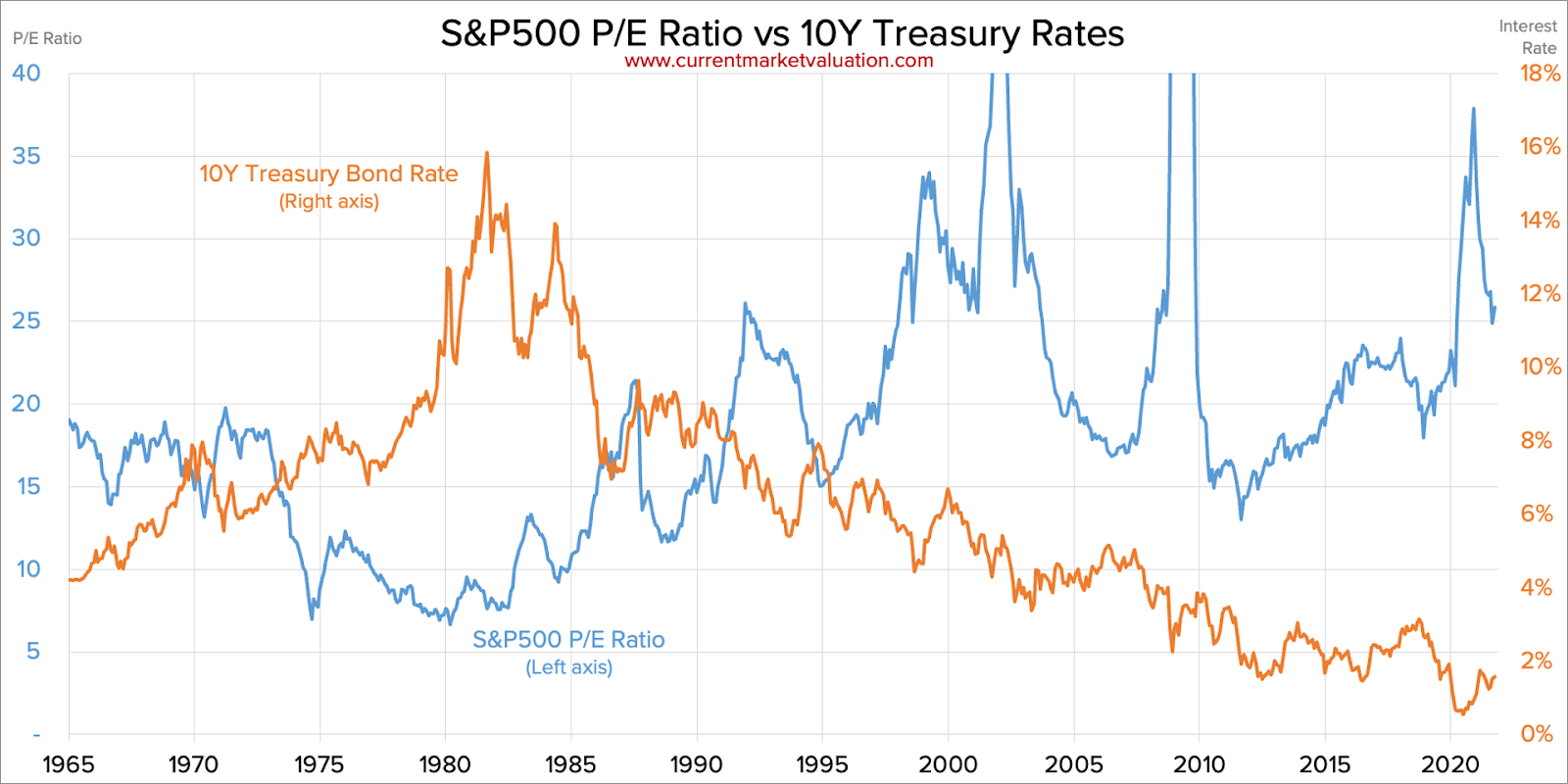

How it works: Policy measures affect consumptions and equity markets directly. Beyond the typical stimulatory effects that you would expect, the effect of low interest rates percolates into the equity markets in a lot of ways. Some affect investors, like the easy availability of margin debt, others affect companies and markets, and we will just focus on a couple– multiple expansion and corporate leverage.

Pic 2: Multiple expansion effects (Data: fred.stlouisfed.org)

This analysis highlights the relationship between the S&P 500 Price to Earnings (P/E) ratio and the 10-year bond yield. While not entirely smooth, lower interest rates have generally coincided with higher P/E ratios over time. This correlation is driven by factors such as increased consumption and growth, reduced cost of capital for businesses, and lower acceptable earnings yields for assets when baseline yields in the economy decrease.

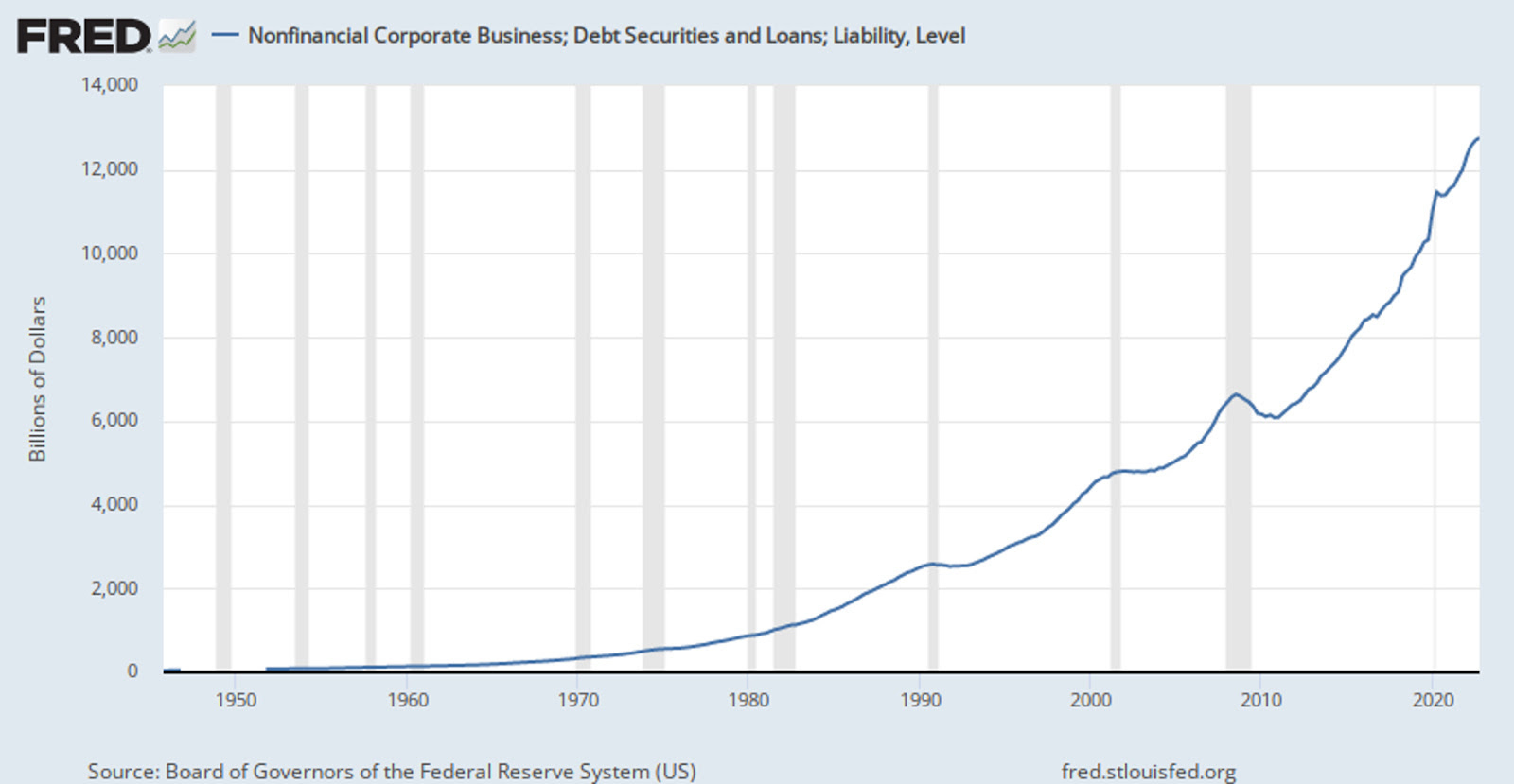

Pic 3: Corporate dept expansion (Data: currentmarketvalutions.com)

Pic: Ad powered by StudioAlpha

Falling interest rates have significantly benefited companies by enabling affordable financing for both equity cost of capital and debt. As a result, non-financial corporate debt in the US has grown exponentially over time, with corporate debt as a percentage of GDP increasing from 30% in 1980 to approximately 50% today. Companies, including major tech firms, have capitalized on these low rates to secure inexpensive, long-term financing.

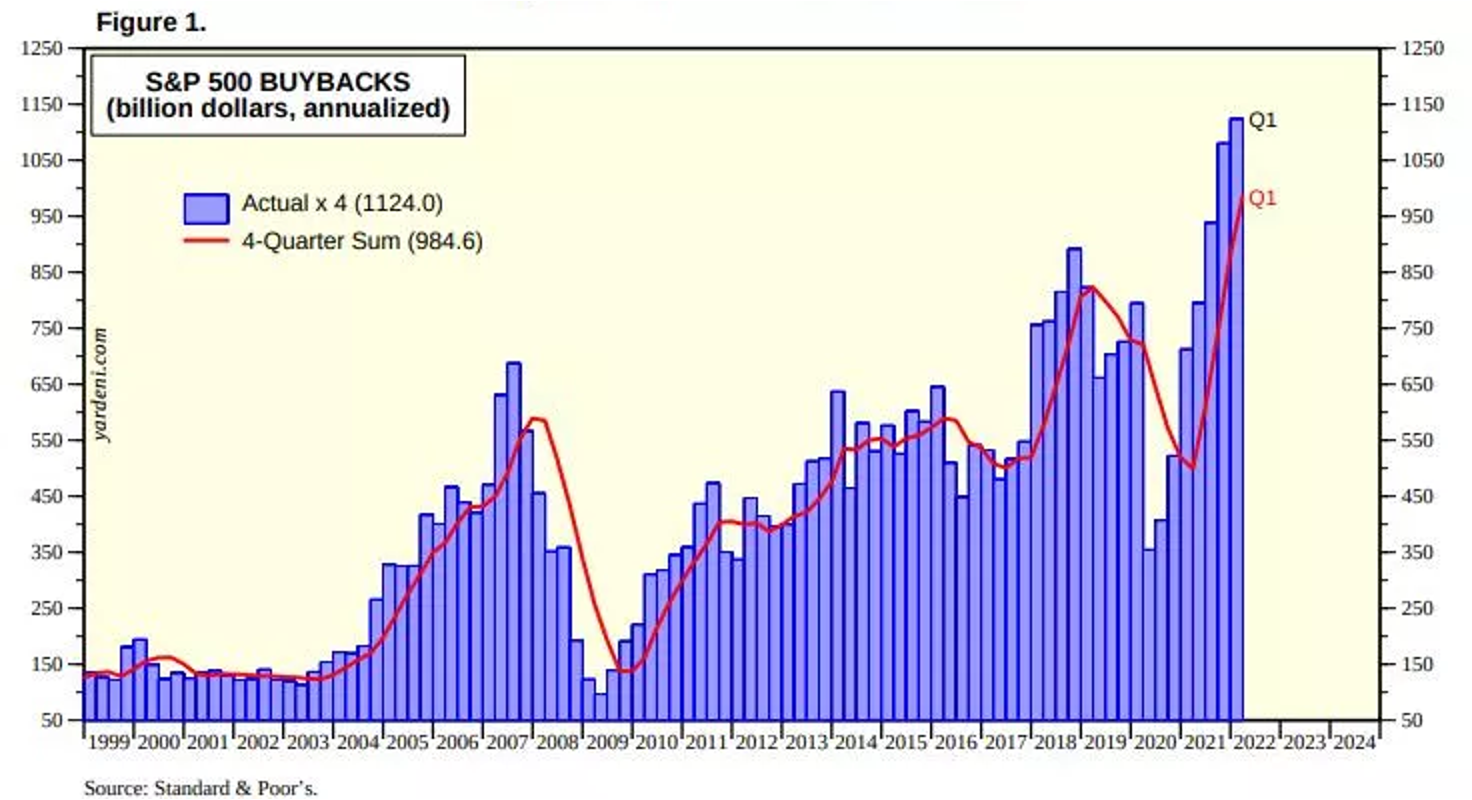

Pic 4: Increasing stock buybacks (Data: Standard & Poor’s)

Exponential growth in corporate leverage has led to increased earnings and enabled companies to buy back their own stock at extraordinary rates. This trend has become a major technical factor supporting the market, with recent quarters consistently setting new stock buyback records. The significant impact of this phenomenon is evident in examples such as Apple, whose outstanding shares have decreased from around 26 billion in 2013 to under 16 billion today.

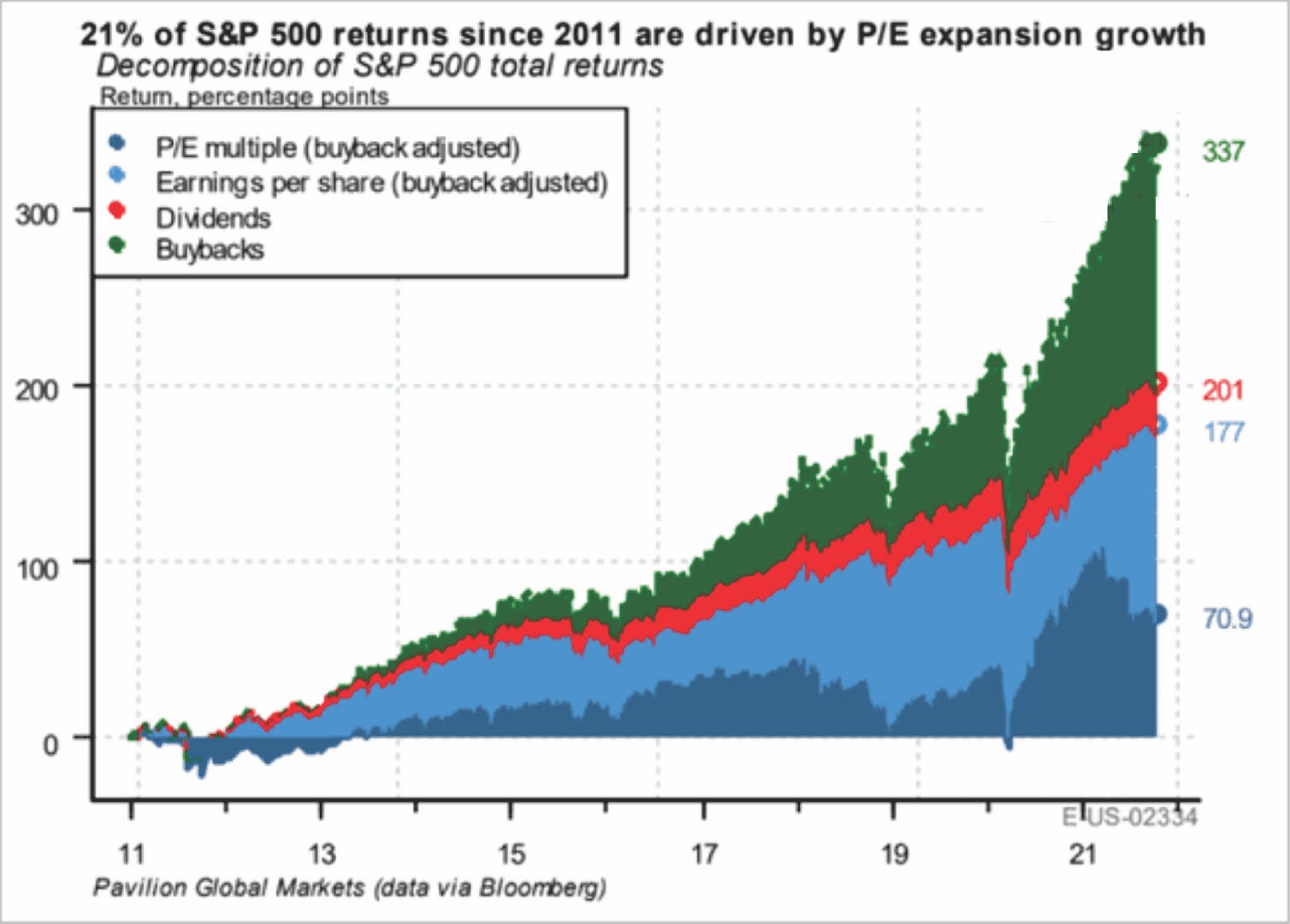

Pic 5: contribution of the above on equity returns (Data: Bloomberg)

The big picture: Multiple expansion and stock buybacks are the primary drivers of stock market returns in major indices, such as the S&P 500. In the illustrated chart, the green area represents returns from buybacks, and the dark blue area signifies multiple expansion. It's important to note that only a minority of returns can be attributed to organic earnings growth, highlighting the significant impact of multiple expansion and buybacks on market performance.

Bottom line: Long-term trends, such as the debt cycle and interest rate downtrend, have culminated in recent years due to the 2008 financial crisis and the COVID-19 pandemic. Low interest rates have fueled higher P/E ratios and affordable financing for companies, resulting in exponential growth in corporate debt and stock buybacks. Ultimately, multiple expansion and buybacks drive stock market returns, with organic earnings growth playing a smaller role in market performance.

The combination of printing excessive money, a pandemic, near-zero interest rates caused inflation and then rapidly raising rates to combat this very inflation has led to a global reset in valuations, particularly affecting unprofitable private tech companies.

Ok, that’s it for today. We’ll back next week. Thank you for reading and posting your questions and feedback!

Best,

Max, Tim & Fabian

Thanks for reading Roll-Right-In! Subscribe for new posts and support our work.

Watch The Clip On YouTube

Join the Roll-Right-In Podcast Community Today

Don't miss out on the opportunity to learn from the best! Subscribe now to our paid weekly newsletter and unlock the secrets behind the world's most successful founders.

A subscription gets you:

weekly subscriber-only posts

participate in polls to influence our content and interviewees

special offers for our events

Content Relations

www.rollrightin.com

f@rollrightin.com

Investor Relations

www.studio---a.com

f@studio---a.com

©️ 2023 Roll-Right-In Podcast / Zurich / San Francisco